Global security breaches are on the rise and no one or country is safe. The acceleration of certain technologies has been rapid since the pandemic engulfed the world last year. But unfortunately, we’ve also become slack in the process.

Once again, it has become apparent just how ‘at-risk’ our data is.

Data hacks have been frantic and are now getting major press attention. It’s hard to know who each unwanted visitor is in each case but fingers are being pointed in perhaps familiar directions.

Russian invaders back at it again

In fact, throughout June, Russians have been blamed for a slew of hacks around the world.

Microsoft in late May said a wave of Russian cyber-attacks had targeted government agencies and human rights groups in 24 countries, mostly in the US.

It claimed that around 3000 email accounts of more than 150 different organizations, some of them international, were attacked in just one week.

Allegedly, the group responsible was the same one that carried out 2020’s SolarWinds attacks, which the Russian Foreign Intelligence Service (SVR) was accused of orchestrating.

But the Kremlin denied having any knowledge or anything to do with any cyber-attacks. It challenged Microsoft to how these attacks were linked to the European attacks.

Nevertheless, authorities are now aggressively investigating cybercrime. In the first week of June, the US Justice Department recovered around $2.3m in cryptocurrency ransom money.

This was part of the funds paid by the Colonial Pipeline Company to Russian hackers in the most disruptive cyberattack on record in the country.

The US deputy attorney general Lisa Monaco said investigators had seized 63.7 Bitcoins which was paid by the company after its systems were hacked, leading to massive shortages of petrol along the US’s East Coast. The department said it founded and recaptured the majority of the ransom.

The hackers are believed to be a group called DarkSide, whose menace caused a multi-day shutdown in certain petrol stations and a spike in gas prices.

The attack made international news and prompted the US’s White House to encourage business executives to improve security measures to avoid future cyberattacks whatever their nature, ransomware or otherwise.

The FBI said DarkSide had also disrupted operations at a meatpacking company. As no one tends to be spared in the spillover effects, it is always a good idea to protect your company’s digital assets as a preventative measure.

Not so sophisticated

The attackers rather proved to be quite ‘amatuerish’ because they sent the Bitcoins to an online platform to convert it to fiat money – and that is how they got nabbed. Server-hosted (Online) crypto exchanges are obliged to keep customer data for compliance and anti-money laundering practices. So while your Crypto digital wallet does not reveal your identity, pairing it with an exchange will link it to all the other particulars you needed to provide to use the exchange.

As long as you need cash to pay for things you will always need to switch your crypto in some way or another – unless your recipient agreed to take payment in Crypto as well. Keeping your digital assets on a hard-wallet or on your hard-drive keeps them “off-the-grid”. But also means you can’t actually spend them.

Although the initial cyberattack was a smart manuever, the attackers proved to be rookies at the robbing game in the end.

On a positive note: the ability to retrieve Bitcoins actually reinforces the need for a Blockchain-based financial system. This made it easier for the authorities to track movements of the ‘ransom-paid’ Bitcoins.

Cuban for a bruising

But politicians aren’t the only people who are urging businesses, civil society organizations, and other groups to improve security systems and be cognisant of an often-dark future.

US Dollar billionaire Mark Cuban has also called for stricter cryptocurrency regulations.

The owner of the Dallas Mavericks who has been investing in trading Bitcoin and other cryptocurrencies such as Ethereum said the world was in dire need of regulation for the burgeoning decentralized finance (DeFi) space.

Cuban said in an interview with Bloomberg that there “should be regulation to define what a Stablecoin is” in order for DeFi to be reliable and to prevent total collapses in investments.

This comes after he saw his investments in a particular Stablecoin ‘went to zero’. Cuban claimed he had been scammed.

Stablecoins are a type of cryptocurrency that is pegged to an underlying asset, or currency – usually the US dollar. They are the earliest forms of DeFi and the largest Stablecoin, Tether, is currently worth more than $62bn.

DeFi has helped the price of Ethereum, the blockchain on which most DeFi projects are built, to also soar. But they can be highly risky investments.

Investors try to create arbitrage opportunities and liquidity between coins but such a scheme collapsed for Cuban.

“There should be regulation to define what a stable coin is and what collateralization is acceptable,” he said.

Buy, Stake, and Trade Cryptos

Strong words of caution

Cuban hasn’t revealed how much money he lost but told a fellow DeFi investor via Twitter that regulation must be implemented- and quickly.

It had been suggested that Cuban was “rugged” which refers to when a project’s liquidity dries up and investors cannot withdraw their cash.

Mark Cuban is alleged to have 60% of his crypto holdings in Bitcoin, 30% in Ethereum, and 10% held in other coins. He likes to experiment with new financial tech investments.

He added further in a recent blog post that banks should be scared of unregulated DeFi technology.

All crypto-based investments remain highly risky as the technology around them develops. But there certainly needs to be global laws to prevent people from losing hefty amounts of their wealth/investment. Cryptocurrency is without a doubt a very lucrative investment vehicle that could make you an overnight millionaire. But that also makes it a perfect vehicle for scammers to clone projects to make away with your hard-earned cash.

You must, therefore, be extra vigilant and scrutinize offers for instant riches. But more so, you would be quite negligent these days to navigate the Internet without any form of cyber-protection.

Maybe you should encourage your kids to become hackers. When you open Twitter handles and Linkedin profiles, it’s not unlikely that you’ll find people listing hacking as a skill.

Parents used to tell their kids to become doctors, lawyers, and accountants. Later, they advised them to learn about computers. These kids have now grown to become hardware specialists and then software specialists today.

In the past 10 to twelve years, we have seen ourselves thrown into the fourth industrial revolution. In it, technology affects our lives through social media and augmented reality.

We share a lot of our personal information with more people, companies, and institutions every day, willingly and are often blasé about it. This has tempted people to steal this information by hacking it.

Hacking background

Since the advent of personal computers in the 1980s hackers have become prolific, initially in ‘first-world’ countries that had an advanced infrastructure. There were numerous cases in the US but as computer technology permeated the world, hackers followed suit.

A hacking group called MOD, Masters of Deception, in the 1980s allegedly stole passwords and technical data from Nynex, and other telephone companies as well as several big credit agencies and two major universities.

The damage caused was extensive and one company, Southwestern Bell said it suffered losses of $370,000 alone. These days the damages, though not always publically announced, can run into a few millions of dollars.

All this has paved the way for a special information technology (IT) vocation. A security hacker is someone who explores methods for breaching defenses and exploiting weaknesses in a computer system and networks. They break into systems they aren’t authorized to, and tend to break seamlessly into email and banking systems.

Advertisment

Hacking as a career

Ben Wilson works as an ethical hacker. He has more than ten years of experience and worked in London where he received on-the-job training. He now works remotely in South Africa servicing UK clients.

“I test websites for clients and look for vulnerabilities in the systems. I have done a lot of work for banks lately but my work is across industries.”

“Energy companies are using my services more and more,” he says.

Wilson says he worked in a permanent position for six years. Right now he contracts for five clients regularly.

Ethical hackers are the knights who test how permeable these systems are.

“The majority of my work is for British clients. The UK pound is strong and I like to earn pounds. I’d say the best computer security consultants in the world are in the UK. The US is strong too but the UK consultants are sophisticated and the best.”

Vulnerabilities

The most common way in which people hack information is through email contacts; especially personal Gmail accounts.

People think that their information is safe because it sits with one of the largest companies in the world. But this is exactly why it isn’t safe.

Gmail and other third-party free email accounts are regularly hacked. If you want to protect especially valuable information you should either upgrade it to the business/enterprise level, use a different email service, or perhaps the one connected to your employer.

Nowadays companies use services to protect themselves against hacks and unauthorized access. These monthly or annual service providers might employ ethical hackers to check the companies’ systems.

Hacking, however, isn’t just something that happens to big companies or in blockbuster movies. Here are some reality checks:

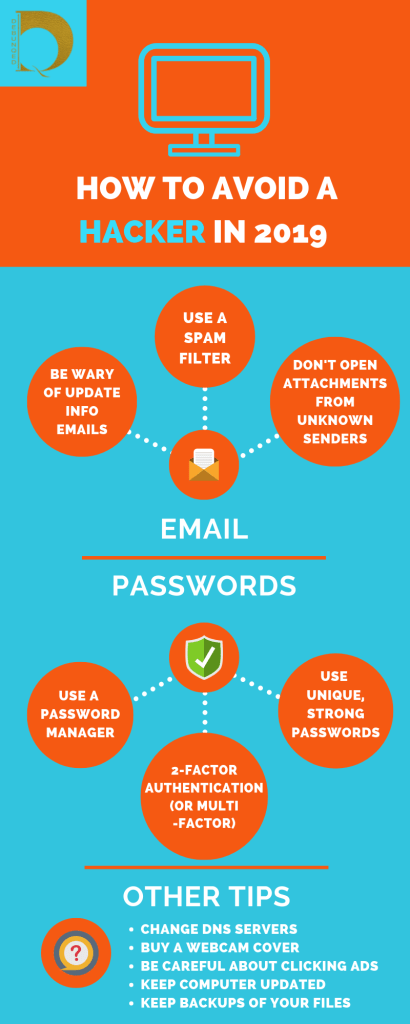

Fortunately, there are several ways of protecting yourself and your information from hacking; starting with your emails. Be wary of “phishing” emails asking you to update your information, especially for bogus databases that you have never heard of.

Use a spam filter – Avoid opening attachments from senders you don’t know – Update your passwords regularly – It helps to have authentication methods, such as a smartphone-linked and email-linked authentication (2FA) or security keys like Yubico – Do not click on any ad – period! Back up your files regularly – it’s always a good idea – Don’t allowransomware bullies to bully you.

If you get sent communication saying that people have your files and want money or they’ll release the files; ignore them.

They can’t threaten you forever and might eventually move onto another target especially if your information loses its value over time.

Anti-hacking software

As a business, use tools like those from cybersecurity experts Acunetix. More than 4 000 companies protect their web applications from vulnerabilities using its powerful web scanner.

Its penetration testing software prevents potential attacks by identifying holes in your websites’ coding. This is where hackers usually plant their complex code which allows them to extract data such as contact details, credit card details, and in worse cases, company-sensitive data like patents and blueprints.

Naturally, it also scans networks to find gateway loopholes that could lead to crashes and downtime-related losses. A bank’s website going down for a few hours can cost it several thousand or even millions in lost revenue.

Despite having firewalls, VPNs,and other Internet security systems in place, your websites and apps being developed are still vulnerable to cyber-attacks or a hack.

The most commonly known hack used is a DDoS attack. Basically, it works like a traffic jam clogging up a highway, preventing regular traffic from arriving at its desired destination. Incidentally, only a few days ago, Amazon was hit by a DDoS Attack.

So, how would you know or find out if you are vulnerable? By conducting regular scans on your websites and apps to see where vulnerabilities lie.

Avoiding a hack requires common sense

Be aware and don’t fall into scams. It’s unlikely you’ve won 120-million Euros in a lottery. You should know by now that you are not the descendant of a king!

In addition, if someone says they have a sex tape with you in it and they want your salary, unless you know you made a sex tape, they’re probably lying.

Unless of course, a scorned lover of yours tricked you – but you can’t blame technology or a hacker for that.

Did you know that there are still more than 700 million people in the world who live in extreme poverty? These people must scrimp, starve, and struggle to survive off less than $1.90 per day.

By 2030, the World Bank estimates that more than 90 percent of those people will be concentrated in Sub-Saharan Africa.

This is perhaps one of the greatest developmental failures of the modern world. Despite the continent’s expansive natural resources and increasing connectivity, foreign actors still feel it’s too risky to heavily invest in their markets.

Blockchain could be the key!

Bitcoin and “Blockchain” were created in the mass wave of distrust in banks after the 2008 financial crisis. Therefore, the technology enables individual, distributed data storage that could become the perfect evidence (trust) base and financial infrastructure for a developing country.

With the right implementation, Blockchain holds the potential to completely revolutionize and revitalize such economies, especially in Sub-Saharan Africa.

So, what is this Blockchain?

Blockchain is essentially a kind of decentralized database that allows you to have a safe, secure way to handle their data without the need for third parties.

For example, you could with Bitcoin, make or accept payments in real-time without needing a centralized bank.

“[It is] a way for one Internet user to transfer a unique piece of digital property to another Internet user, such that the transfer is guaranteed to be safe and secure, everyone knows that the transfer has taken place, and nobody can challenge the legitimacy of the transfer,” said software entrepreneur Marc Andreessen.

“The consequences of this breakthrough are hard to overstate.”

Historic background

Until the mid-twentieth century, most of Africa was ruled under a colonial system meant to exploit the people and their natural resources for European benefit. Africans, in addition, were rushed into development according to European standards rather than homegrown ones.

The legacy of rapid development, distrust and corruption left behind an economic system failing to recover in the 21st century.

While the World Bank celebrates a decrease in global poverty levels, the number is expected to remain stagnant in Africa. Today’s poorest people are living in places with the least economic growth.

Sadly enough, poverty and lack of investment in many developing countries stem from how they were integrated into the world system.

The land was cut into countries according to European treaties and agreements, rather than by traditional and tribal land divisions. This situation worsened upon the handover of colonial power to so-called “democracies.” Power often shifted to the ethnic groups that former colonizers favoured.

Corruption multiplied in the form of bribes, political persecution, rigged elections, and a massive wealth gap. All of this still affects the wealth distribution and investment potentials of many developing countries.

Of course, this created a lack of trust in banks and government throughout much of Sub-Saharan Africa.

The perfect fit for Africa

During a 2012 study conducted in rural Western Kenya, Stanford University researchers waived the costs of opening basic savings accounts for a number of unbanked individuals.

While 63 percent of the subjects opened an account, only 18 percent of them used the accounts. This was likely due to three factors: a lack of trust in banks, unreliable service and prohibitive withdrawal fees.

Unfortunately, the prevalence of unbanked individuals in the informal sectors scares off foreign investors, who heavily rely on transactional evidence to make investments. Otherwise, pouring money into markets is too risky. That’s where Blockchain comes in.

How would it work?

Blockchain can host an entire evidence base of transactions, loan repayments, and asset titles. The technology is also decentralized and requires individual confirmation, creating an element of trust and transparency beyond traditional banking systems.

According to Victor Olorunfemi, Director of Products for Pan-African tech and crypto-exchange, KuBitX, Blockchain’s major benefits lie in “frictionless P2P and cross-border payments, transparent elections, land registry management [and] transparent crowdfunding.”

Let’s look at some of the different ways Blockchain could benefit developing economies, especially in Sub-Saharan Africa.

1. Creating financial infrastructure and accountability

According to a study by the Milken Institute, viable financial markets require consistent, accurate data on assets and credit histories. Luckily, Blockchain may fulfil these needs.

The use of Smart Contracts technology is ideal in areas lacking accountability, such as the real estate or land/agricultural sectors. In Africa, a lack of record-keeping practices often leads to “missing” or non-existent title deeds. In some cases, this is intentional.

Title deeds “go missing,” only to end up in the hands of benefactors other than the rightful owners. Smart Contracts could eradicate these issues through the use of special tokens that cannot be duplicated, changed or removed. See the article on tokenization.

Likewise, Bitland, a company in Ghana, currently helps individuals record deeds and land surveys. By resolving land disputes, Bitland creates more stability while accurately recording land asset data.

“There’s a massive number of people in the informal sector, but there’s not much data being collected on them right now.”

Merit Webster, co-president of the MIT Sloan Africa Business Club.

“That means you don’t have that credit history or payment history for them. If you have a decentralized approach to collecting data, you end up with more malleable data. [This] is very valuable for creating credit histories.” The agricultural industry also has the potential to thrive using Blockchain.

“Blockchain could be used to track goods around the world. This allows farmers to earn a fair wage for their goods.”

Also, farmers could use record-keeping technology to streamline the supply chain and document resources. This would lead to better efficiency, lower transactional costs, and improved logistics.

2. Security in banking

According to the World Bank, there were 1.7 billion people with no bank account in 2017. This situation is worst in developing countries, especially African ones. For example, over 62 million of these people lived in Nigeria.

Besides, data from Google Trends reveal that Lagos, one of Nigeria’s biggest cities, ranks globally as the number one city based on the volume of online searches for Bitcoin (BTC). Clearly, for the city’s 21 million-odd people, there an immense interest in some form of an accessible payment system.

Of course, it’s unrealistic to expect bank branches to magically appear in every remote corner of the world. However, a digital database using Blockchain technologies has the potential to reach far beyond physical banks.

Ad: N26 Bank

Many Africans value trust and transparency. In developing countries, this lack of trust goes beyond the Internet. Developing countries with less industrialization tend to have higher levels of corruption.

This reduces national investment opportunities in the public sector and instills a lack of trust in centralized oligarchs handling an international investment.

Because its power lies within the community of users, Blockchain can combat these trust issues. All data logs and amendments must pass through this community and identification confirmation tests.

Blockchain technology also secures your data incredibly. Hacking and data breaches are all too common nowadays. In 2017, for example, around 3 billion Yahoo user accounts were stolen.

When information is stored in the same place, hackers have one, easy target. In contrast, Blockchain is a distributed entity. This dissemination of data leaves it far less vulnerable to cyberattacks.

3. Fostering Entrepreneurship

Coupled with the Internet, Blockchain technology could be the perfect platform for aspiring African developers. Because the ‘source code’ is free of charge, skilled coders can adapt, create, and configure special applications, called DApps.

These are available on Crypto platforms and provided by companies like Ethereum, and a South African firm specializing in what they called the Keto-Coin.

Rather than waiting for governments to drag their feet trying to create jobs—individuals on the continent can form small firms that build and sell Crypto-based Apps locally or abroad.

“Despite the frictions and impediments mentioned,” said Olorunfemi. “Blockchain can still provide an avenue for promising African tech projects to access capital (FDI) via token offerings on digital assets exchanges.”

Many courses are even readily available online to quickly learn about new technology. Microsoft, for instance, offers a platform via Azure for you to build and learn about the Blockchain.

One-man shops in countries with unfavourable economic systems, like Zimbabwe, can also adopt smaller, stable, Cryptocurrencies to facilitate or payments. In cases of rampant inflation, they can temporarily act as a store of value or help you pay for things until your currency stabilizes.

As with the Venezuelan hyperinflation case study, Cryptocurrency intervention could help many developing countries troubled with economic instability.

There is also the option of Crypto-mining. But before you pull out the ‘high-consumption energy’ argument – think outside the box for a moment. What about energy sources that are free and available nearly 24/7? Like water and the sun!

The African continent is full of capable scientists and mechanical engineers. One could build special solar-powered energy centers to power Bitcoin-mining.

And without the expertise, governments or private companies could alternatively just invite Crypto companies with abundant financial resources to mine (cleanly) for a special tax/fee while creating jobs for the locals.

4. Elections

In addition to the financial side of things, Blockchain technology could help eliminate some forms of corruption. For example, many African countries’ elections are incredibly vulnerable to the social scourge. In some extreme cases, some officials change or forge written ballot votes to rig elections.

To combat this, Blockchain databases could record votes. This makes it nearly impossible to tamper with using Smart Contract technology. Having fair elections improves infrastructure, which then increases development and economic dependability.

While some might see Africa’s economy as underdeveloped, others might see it as a blank canvas well-suited for a large-scale implementation of Blockchain. Economic and governmental systems are shifting and slightly shaky in many Sub-Saharan African nations.

The challenge is to foster a rigid economic system to implement Blockchain.

Don’t just take our word for it—African nations have often implemented new, practical technologies before the Western world. Let’s look at the example of M-Pesa. Back in 2014, Americans and Europeans were amazed by Apple Pay’s launch.

However, this mobile payment system wasn’t exactly “new.” By that time, Kenyans had used M-Pesa, a very similar technology, for years.

“There’s a lot of opportunity to leapfrog the way the West developed and have these more unique African solutions, but it needs to come from within,” said Webster.

“It needs to come from entrepreneurs in the continent who want to implement these solutions. It’s important to engage people very early on. Systems incubated in the West don’t stand as great of a chance to work as African ones do.”

Concluding remarks

With the possibility of an experimental, large-scale takeover of Blockchain technology to improve African infrastructure, the nations there could leapfrog in development and growth.

This must begin internally. According to Olorunfemi, “Education—of policymakers and other stakeholders—which is often ignored has to be a critical factor in paving the way for the acceptance and adoption of new technologies and the accompanying investment.”

The results in Sub-Saharan African countries could help eliminate much of the world’s poverty. It would also remove remnants of mistrust and corruption left behind by the days of colonial exploitation.

While there are some obstacles to large-scale Blockchain implementation, we can’t think of a better benefactor than there. The possibilities for business using the Blockchain are endless!

To learn more about how to get started with Cryptocurrency mining or purchasing, visit our resources page for useful links and guides.

Additional input by Bobby Quarshie (BQ).

Citations: Christopher Lee and Jackson Mueller.

Swan, Melanie. “Anticipating the Economic Benefits of Blockchain.” Technology Innovation Management Review 7.10. Oct. 2017.

Bitcoin Lessons from Venezuela, Where Hyperinflation Reigns. Online Source: https://www.lathropgage.com/newsletter-237.html

Like a biological virus mutates – as technology advances so do the complexity of phishing and identity theft schemes. With major services adopting cloud technologies and storing private data online, anyone is vulnerable to hacking.

To make matters worse, hackers continue to come up with some pretty creative ways to profit from stolen information.

Without wasting time, these are the things you should already be doing to avoid being exposed to hackers in the first place:

In order to keep these cyber-criminals out of your lives and computers, let’s take a look at some of the actual schemes to watch out for in 2019.

Hacking

We all know what hacking is by now – the term has almost become synonymous with internet security. So a question is: do you love watching movies on Netflix or jamming out to your summer playlist on Spotify? If the answer is yes, then you’re at a pretty high risk of getting hacked.

DynaRisk, a UK cybersecurity firm, recently found that cybercriminals most commonly target these brands, along with adult-oriented sites (you know what we mean) and then, online gaming services.

Identity Theft

A few weeks ago, authorities caught a New York-based gang who had used identity theft to steal over $19 million worth of iPhones. Quartz reported that this operation ran for seven years.

So-called “Top Dogs,” the ring leaders, would organize lower level members of their organization to steal identities and create clone credit and identity cards. Then, affiliates fanned across the nation, signing up for mobile phone plans to acquire iPhones, which were later sold for a profit by the Top Dogs.

Because phone payment plans take the shape of nominal fees over the course of several years, victims often wouldn’t notice the fraud until it was too late. Learn how another scheme dubbed sim port attackworks in the diagram below:

Ransomware

Hacking can happen to anyone – including our favorite bands. In early June, a hacker managed to steal the minidisk archive of Thom Yorke, the lead singer of Radiohead. This included previously unreleased demos and audio material from around the time of “OK Computer,” the band’s 1997 worldwide hit album. The hacker then demanded $150,000 on the threat of releasing it.

Holding files for ransom is so common nowadays that it even has its own name: “Ransomware.” Either pay over the ransom or lose your files—or, even worse, have them released onto the unforgiving Internet.

In response, Radiohead released all 18 hours of material on Bandcamp themselves, winning against these ransom hackers.

Most security experts recommend the same route as Radiohead—never pay the ransom, because there’s no guarantee you’ll recover files or prevent their release.

Sextortion

If you think ransomware is bad, there’s an entire subgroup of it aimed to profit off sexual shame. Cheekily named “Sextortion,” some hackers creatively upgraded the classic email phishing scam to scare victims into handing over Bitcoin.

According to Fortune, hackers have already racked up over $900,000 with sextortion. In these phishing emails, the sender claims to have spied on you while you watched porn—and has webcam footage of the salacious deeds. The message then demands a Bitcoin ransom, or else face the social and professional consequences of this lewd video getting sent to all your contacts.

To make the threat even more believable, the sender references a previous password tied to the user’s email account. According to Krebson Security, a sextortion phishing message might look a little like what’s written in the sidebox.

In rare cases, the threats are real—and hackers get their hands on some sexually explicit photos. Recently, American actress Bella Thorne fell victim to sextortion. Last Saturday, she took a similar, albeit more risqué, route as Radiohead, opting to release her nude photographs on Twitter in order to take the power away from her hacker.

Last thoughts

So, what’s the best way to avoid your personal, or, business from costing thousands in virtual currency? Since most of these emails are fake, you can just avoid them with a spam filter. And you should probably buy a webcam cover…just to be safe. When it comes to general browsing- we suggest using a VPN.

There are now more secure anti-hacking tools that use the Blockchain and offer great protection, especially against identity theft. Have a look at our feature on Tokenisation.

Most online services now like mobile banks, offer App-based 2-factor authentication. This should now be regarded as the minimum security for ANY online account or App.

To avoid hacking or phishing scams in general, optimizing your cybersecurity and using online common sense will save you loads of time, trouble and money.

We have barely scratched the surface with the Internet (from the early eighties) and it is already seemingly being threatened with the competition. A possible replacement by a new phenomenon.

Well, for lack of a better word, “replaced” has connotations of a dying Internet. This is far from accurate. This new phenomenon – fostered by blockchain technology, will change the way we use and consume the Internet as a service.

So, what is this new Internet-like system creating waves online? And why is it making online marketers quiver at the prospect of them losing out on the exponential revenues they have previously enjoyed?

Before we delve further into its meaning and use in the cyber world, perhaps some background context is required.

The way we use online or mobile applications software or “Apps” has changed how we consume products and services online. Companies jumped onto the bandwagon when they discovered that we mostly use Smartphones for the Internet.

App developers were then subsequently sought after to create mobile Apps for practically anything. What started as something mainly for gamers moved quickly onto applications for practically any commercial activity.

We now use Apps for our shopping; fitness; traveling; online bookings and banking. Developers now create customized software to help us with practically, anything.

In addition, we now have App stores for every significant tech provider – Microsoft, Google, and Apple to mention a few. This has naturally fattened the pockets of software companies and created an additional stream of income for them.

The ‘catch’ for using mobile apps is that even though it costs you nothing to download, using them still requires you to register with your personal details. You can also do this by linkingyour existing social media accounts.

The benefit to App providers

These Apps, which are integrated with social media services, create a data goldmine for marketers to study and track browsing habits. Through them, marketers can gain valuable insights into your interests and then customize their products/services to sell to you.

The impetus behind a distributed application system is that it serves to distribute plow some of the wealth garnered from your data via application providers back to you.

Data mining has become more lucrative and accessible because of Artificial Intelligence (AI) and Machine Learning. Do you ever notice how after browsing online or having a conversation or a chat application like WhatsApp or Facebook Messenger? You go online later, and you see Ads displaying the items you discussed? Creepy isn’t it? Well, that is the future of Web 4.0 for you!

Staying ‘woke’

Luckily for us, there is a school of knowledgeable and security-conscious programmers who are not ‘giving in’. They help us understand how the Internet has become a cesspool for marketers to harvest our data. Social media platforms, search engine providers, and mobile application providers facilitate them immensely with this.

Imagine getting paid to surf the web for hours. The way you get paid for taking on a survey, partaking in a social experiment, donating an organ or sperm?

This is the way distributed apps are touted to work. They reward you for the use of specific applications (in a peer-to-peer review setting) with cashable tokens. Seems only fair right?

Now you can imagine how companies like Cambridge Analytica would react to having to pay you for their use of your data. They would surely be reluctant and that’s why they preferred to work clandestinely. But if they could pay companies like Facebook for the use of data, why not pay us directly?

Early adoption

Joining the ‘DApps revolution’ is a no-brainer. Those at the forefront of building and supporting DApps will end up with a more substantial chunk of the market.

DApps primarily provide you with the use of payment systems. These are specifically known as Smart Contracts and Proof of Work systems.

For instance, you are rewarded in cashable tokens to surf the net over applications like Google Chrome, or Mozilla Firefox.

It is only a matter of time that this form of Internet-browsing and use of applications becomes the norm.

The Internet revolutionized the way we communicate, socialize, learn, shop, and do business online. DApps however, will determine the way you get compensated for doing the things you love to do online.

There is a lot of banter, which is backed up by well-research papers on how Automation and Robotics (powered by AI) will replace manufacturing jobs.

Blue-collar jobs are not the only ones however, that face imminent and progressive extinction.

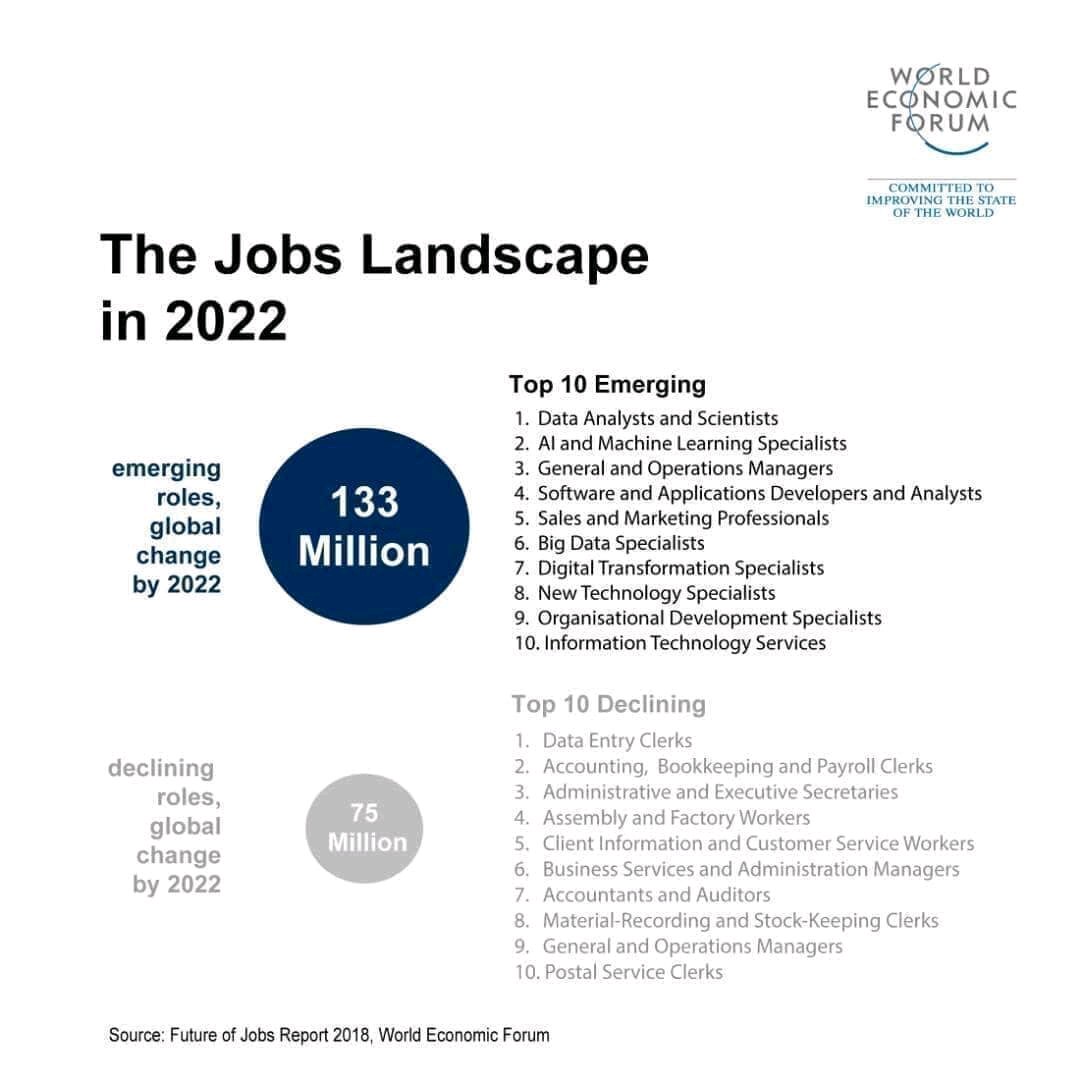

A recent survey report conducted by the World Economic Forum predicts futuristic trends affecting certain jobs in the modern workplace.

Robert Solow predicted decades ago, in his Solow-Swan model, a massive driving force of global growth: technology.

And the evidence is prevalent with the likes of Apple, Google, and Amazon championing stock markets with Billion-dollar market capitalizations. They also create an abundance of jobs globally.

Disruptive technological advances such as AI(Artificial Intelligence); the ubiquitous high-speed mobile Internet (5G); widespread adoption of big data analytics; cloud technology; and the recent Blockchain technology will be the drivers of this job evolution.

Based on the report, by 2022, this job evolution will be firmly in place as it has already.

In a matter of just 4 years, we could have a situation where jobs such as postal service clerks, data entry clerks, and bean-counters (accountants and auditors) would be made redundant.

Impact on services

Software like Microsoft’s Dynamics 365, aims to remove ‘silos’ within customer relationship management (CRM) and enterprise resource planning (ERP) processes.

The latter takes over (fully automates) back-office operations such as stock-taking and supply chain management.

Such tasks will be performed via software, reducing the need for more human supervision. Consequently, the focus would be more on managerial roles.

In the sales and customer service realm, technologies like Microsoft’s AI will provide automated insights to guide employees on improving customer experiences.

Furthermore, it may lower support costs by using virtual agents or Chatbots to eliminate in-house AI experts and those writing code. This will result in more redundancies!

On a positive note, newer and more exciting jobs such as data analysts, machine learning and AI specialists, digital transformation experts and in general information system services will be on the rise – up to 135 million globally, according to the Report.

The fields to benefit directly from new technologies would be information technology; information security; innovation; customer services and risk management (financial services).

Impact on finance

Another group of professionals whose nature of work will be affected due to the advent of ‘disruptive technology‘ is financial middlemen. Likewise, smaller banks and money transfer institutions.

Decentralized systems were primarily put in place to eradicate exorbitant fees associated with transferring money across borders.

Cutting them out completely undoubtedly renders them redundant. It is therefore pertinent for them to innovate their products in order to open up sufficient job position.

Recently, Malta’s finance minister whilst in a private interview during a Blockchain Conference, echoed this. He said that the advent of cryptocurrency has changed financial middlemen into traditional “photo developers”.

“I can see this, just like in photography when you could tell that […] those who process the photos will lose their jobs; a lot of financial intermediaries will be facing the chop in the not too distant future,” says Edward Scicluna.

The good news for governments will be that the trend shows that the jobs created will surpass those lost.

Be proactive and skill yourself accordingly or get the right personnel who can quickly adopt some of the mentioned skills so that you do not fall behind!

When considering small business financing, it is important to understand all your available options. If not, investors can easily take advantage of you and offer unfair terms.

So before raising any money, find out if using equity, debt, or convertible debt financing makes the most sense for you to grow your business.

Equity

Raising capital through equity is popular, if not the most popular choice, for entrepreneurs to pursue. Investors buy stock (or shares) in your company, giving them a financial stake in the future success of your business.

How It Works:

You set a specific Dollar/Euro amount for what your company is worth.

Based on that valuation, investors agree to give you money in exchange for a certain percentage of your company.

Investors receive compensation based on the percent of stock/share they own once you sell the company or go public.

Pros:

All your cash can go toward your business rather than loan repayments.

Investors take on some risk and don’t have to be paid back until you’re doing well.

Investors often have valuable business experience.

Since investors have a financial stake in the success of your business, they are motivated to offer sound guidance and valuable business connections.

Selling shares of your company will make it very difficult to get them back.

You will also most likely lose control of part of your board to your investors.

Debt

Debt-based fundraising is the form of small business financing that most small businesses end up choosing, according to Fundable. It is also the easiest to understand. Money is loaned to you with the agreement you’ll repay it over time with an established interest rate.

Get a quick loan for your business here:

How It Works:

You borrow money with an agreement to pay it back with interest within a specific time frame.

You will also have to offer your lender some form of collateral, which are liquid assets you will give up if you cannot make your loan payments.

Pros:

You will raise capital much quicker than with equity small business financing. This is especially true of smaller cash amounts.

You can keep 100 percent ownership of your company, along with 100 percent of its profits.

Interest payments are tax-deductible.

Cons:

You must be completely confident you can make your loan payments in cash each month. If you don’t, lenders can make you sell your business in order to get their money back.

Interest payments can become one of your largest business expenses.

Commercial lenders will demand small business owners to personally guarantee the loan and offer personal assets as collateral. This even if your company is structured as a corporation or limited liability company, according to Forbes.

Convertible Debt

A convertible debt small business financing structure is a mix of debt and equity financing. The money raised is considered a loan, but at some future date, the loan can convert to equity if the lenders so choose.

How It Works:

You will negotiate an interest rate to pay back the loan. This will also be the interest rate for those lenders who decide not to convert any debt into stock.

The details concerning how lenders can convert the debt into equity are negotiated at the time of the loan. For the most part, that means agreeing to give lenders a discount or warrant on an upcoming round of equity fundraising.

You will also set the valuation cap, or maximum company valuation, at which lenders can convert debt into equity. If investors decide not to trade in their loan for shares at this predetermined valuation level, they can no longer do so at a future date.

Pros:

Transaction costs are low and the process moves quickly.

If you don’t want to set a company valuation, which involves a lot of uncertainty and risks for new startups, a convertible debt structure for small business financing makes a lot of sense, according to Covestor CEO Asheesh Advani.

Using convertible debt protects investors from dilution in future financing rounds.

Cons:

Investors are uneasy about giving money without knowing the exact share of a company they will own. You might have to offer steep discounts on equity in order to get them to agree to the terms.

You may be forced to set a valuation before you are ready in order to avoid unaffordable loan repayment expenses.

In the end, it’s best you make your final choice, based on which of the mentioned options works best for you, not just now, but in the immediate future.

UpCounsel is an interactive online service that makes it faster and easier for businesses to find and hire legal help solely based on their preferences.

As much as institutions, risk-averse, or simply skeptical people have downplayed the new digital currency revolution. It still, a decade after coming to public light, remains resilient.

Bitcoin now gets a regular mention in daily news and stock market reports. It is being traded by several established investors and even included by fund managers as high-risk portfolio instruments.

We all by now, have heard the rhetoric of high volatility and use for criminal activity when it comes to Bitcoin and its crypto-family.

Billionaires Warren Buffet and Bill Gates also weighed into this by publicly lambasting Bitcoin. Buffet equated cryptocurrency to rat poison 🙂

Be it may, digital currency, however, does have some unbeatable benefits and functions you cannot ignore.

Financial emancipation

Bitcoin and ‘altcoin’ investing have created a new wave of financial investors.

These include retired bankers, ‘millennials’ – who instinctively jump on-board a new discovery that has creative destruction-like tendencies. You also have the plumber, bartender, or ‘average man on the street’ looking to change their lifestyles instantaneously.

Based on their phenomenal returns, many people have taken to social media (via groups, profiles, and communities) to share their success stories. But this is also a reason to for you to heed caution when you take counsel from anyone claiming to be an expert in cryptocurrency investment.

Volatility is not new to trading – and especially not with Crypto trading. It is constantly on a rollercoaster ride making it hard for even seasoned trading experts to predict movements with traditional market analysis tools.

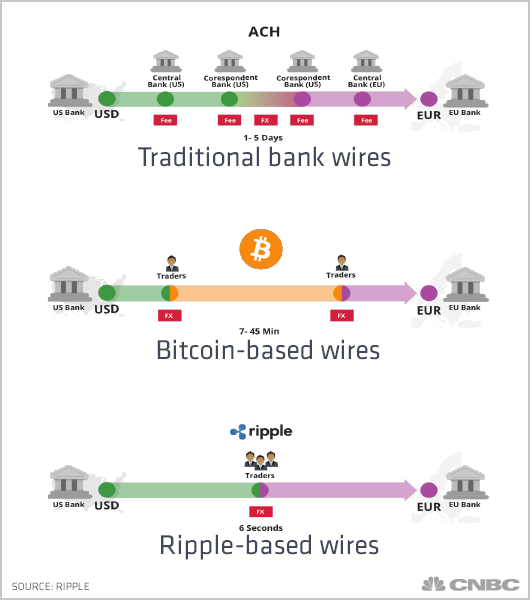

Money transfer

We all have undergone the painful stress of waiting for funds to clear so your rent gets paid or waiting endlessly to receive money from abroad.

With cryptocurrency, the aim is to be not only the most secure form of funds transfer – but the fastest.

Converting cryptocurrency to fiat money, however, remains a bottleneck. It still needs institutions to adopt or directly accept payments in cryptocurrency to avoid you going through another step in order to transact.

Cryptocurrencies still cut down transfer time significantly compared to traditional electronic fund transfers of fiat money.

Some well-established companies already use Cryptocurrencies like Bitcoin, and Litecoin for fund transfers, or even direct exchange for services.

Cost savings

We cannot ignore the reduced costs associated with dealing with money you have (hopefully) earned from hard work.

Even inheritances are gained because of the toils of the giver’s hard work. So, it wouldn’t be fair for a group of a few companies headed by executives to siphon it from you while claiming to ‘provide you with a service’.

We all pay for Internet use (and the security software associated), for smartphones and computers.

We, therefore, have the technology to make transactions ourselves without having to rely on others to charge us for things we can do ourselves.

The financial institutions have long preyed on your ignorance, obedience, and unquestioning trust. This, while they brazenly burn cash dabbling in equally questionable high-risk investments like derivatives and futures.

Use cases

Cryptocurrencies have nevertheless, got us thinking about making profits, the tax implications, and anything financial for that matter!

A recent development called Hodl Waves attempts to track and predict Bitcoin movements via complex usage history. It basically compares behavioural patterns of what you do when you have coins and when you choose to reinvest them.

Blockchain technology has also spurred a new path of careers and industries. More companies globally are looking to acquire lucrative Crypto-exchange licenses to operate.

These cryptocurrency exchanges require people to service clients in various areas. They will require employees as any company would.

Governments too will benefit from their operations. While there are still discrepancies in most countries about how to tax you, authorities can get a lion’s share from directly taxing exchanges.

A new wave arises

It is only a matter a time before the banking institutions and big companies get on board to benefit from the high-level encryption and speed provided by digital currency.

To conclude, the ‘wait and see’ mantra is all that we can exercise when predicting the future of digital currency.

There are, however, concerns on how secure the encryption can remain with the advent of quantum computing. This ground-breaking tech can make calculations at millions of speeds faster and thus able to crack the toughest data encryption.

Some form of regulation would be required in some form to keep Crypto prices stable.

Warren Buffett once referred to financial derivatives as “weapons of mass destruction” . He warned that they are detrimental to the global economy and financial markets.

Cryptos have a way of creating something supposedly of intrinsic value out of nothing. This is as dangerous as propaganda that leads to conflict or promotes struggle.

They are backed up by a cloud of non-regulatory policies by states who themselves, still traditional monetary policy measures.

And this is despite their full understanding of the instruments of financial wizardry.

In economics, the term creative destruction, however, has a paradoxically positive meaning. It is perfectly suited to the new form of “crypto”- currency (Bitcoin) that is not as mystic as it seems.

A brief history

Money is a concept that probably also met up with resilience when it was first supposedly introduced by the Chinese. They started carrying folding money during the Tang Dynasty (A.D. 618-907).

The instability generated by uncontrolled usage and denomination, however, soon led to rapid inflation. This prompted the Chinese to drop it, only for it to be taken up again later when it got stabilized by the adoption and use by the West.

They developed paper money as an offshoot of the invention of block printing. Block printing is like stamping.

Ironically that very same term ‘block’ is the foundation behind the Bitcoin – which is generated using blockchains (digital public ledger).

We won’t get into the mechanics of Bitcoins. We will, however, attempt to increase awareness on why and how this new payment method could cause positive ripples in the financial global system.

What is Bitcoin?

As per Wikipedia, and as simple as it can get in terms of a description: Bitcoin is a cryptocurrency and a digital payment system.

It was supposedly invented by an unknown programmer, or a group of programmers, under the alias Satoshi Nakamoto in 2009.

Though the anonymity creates an element of distrust about the agenda of its creators, it is surprisingly more transparent than derivatives.

Cryptocurrency uses a system of cryptography (encryption) to control the creation of digital ‘coins’ and to verify millions of transactions.

These transactions include are a basic movement of funds between two digital wallets and get submitted to a public ledger and await confirmation through encryption.

This video is a great and simple way for you to understand the above because it is best understood when explained as a larger picture. Check out this useful and basic video on Bitcoins.

That is quite a feat worth acknowledging because 11 years of existence is nothing compared to gold’s multiple century reigns.

Now 2009 was not long ago considering the Bitcoin is now ‘worth’ well over $20 000 each (updated to 2021 levels).

For centuries, gold has been our standard of trade or backing of all types of currency until it was ‘uncoupled’ by Nixon in 1971.

The future of trade and commerce is in the digital sphere – are you in the know?

Potential currency?

For something to become the standard measure or mode of trade it, however, needs to be stable. So, while the technology behind Bitcoin (the Blockchain) is relatively sound, its actual price needs to find its firm nesting.

Established currencies trade on markets via exchange rates with relatively minuscule increments of change in price and value. In comparison, Bitcoin can jump in value by $1000 within (minutes or seconds) – prompting skepticism about its stability.

Google Engineer Ray Kurzweil, who is revered as a “prophet” for his mysterious predictions, such inconsistency undermines the cryptocurrency’s value as a currency.

The aim is nevertheless to relieve our dependency on money or more so, the iron grip and often abusive control that some banking institutions have over consumers.

You could even argue that the recent surge in its price is being fuelled by agents of the traditional banking industry. They naturally feel threatened by the fact that they may not fully understand it and its inherent potential. So they (cash-flush) could inflate it for an inevitable ‘burst’.

But the currency though very volatile in its movement has remained buoyant. It has now held for well above $10 000 for sustained periods since its inception. Gold is now approx. $1,900.

Bitcoins provide more guarantee than financial derivatives especially because of their open-source approach to its existence and use.

Complexity

The tricky part is simply getting to grips with the vastly abundant information about it and how you could even generate it.

It is still a great backup ‘of a backup’. We rely on technology and more specifically the Internet for transactions and the associated traffic for our daily lives.

A simultaneous crash of a few major servers, however, could send it all tumbling back into the digital abyss. But as with money and other forms of currencies, only time will tell.

Bitcoin will just have to further prove its resilience and stability in the long run.

Getting attention

It is certainly not a ‘fly by night’ thing because it has sparked the interests of both public and private institutions globally. China even made a bold move to block the Bitcoin market from trading within its borders at some stage.

Bitcoin also gets its collective strength (intrinsic value) from its limited quantity in circulation (19 million out of a finite 21 million).

Spillover effects

Bitcoin has also paved the way for others such as Ethereum, (mostly used for smart contracts and by developers) which is also seeing good growth. Then there is Litecoin, which was formed as part of a controversial yet civil split from the originators of Bitcoin to use ‘variant technologies’.

All these platforms (companies) now use the blockchain to create all types of cryptocurrencies to capitalize on the spoils of this digital revolution.

There are also several institutions that are offering late-comers a chance to benefit from the spoils of using and investing in digital currency.

Naturally, all these schemes with their investment packages would require a ‘buy-in’ and marketing to attract more takers.

Such Crypto ‘companies’ are likened to a pyramid scheme and subject to many investigations by fiscal and criminal authorities. But that is how Bitcoin, its promoters, and the market were initially treated.

Interested? Check out the following useful links to their official websites to help you get started.