The world is slowly realizing that it needs to rely less on old systems in order to manage its way out of financial crises. One of the oldest systems which saw the US dollar as the vehicular currency of the world may be slowly coming to an end.

Enter the Bitcoin: the brainchild of cryptocurrency, a means of exchange that is less regulated and which is built on the Blockchain, a technology that is supposedly difficult to hack into.

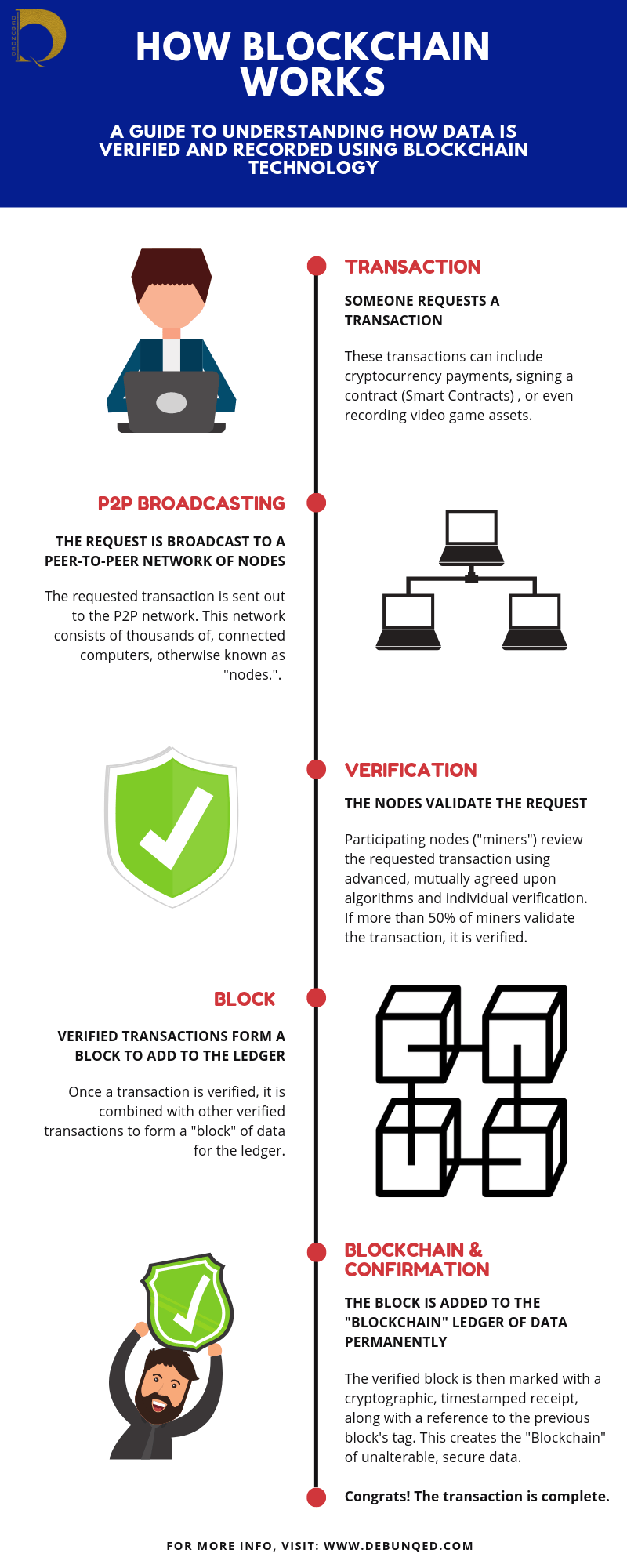

A quick recap for those of you not familiar with the tech: A Bitcoin is a computer file that can be stored in a ‘digital wallet’ app on your smartphone or computer. With this technology, every single transaction you make is recorded in a public list or publicly distributed ledger.

This makes it easier for authorities to track and record your transactions but not you personally. We will not, however, get into the potential abuse of such anonymity in this article.

Adoption

We have been very slow to adopt new financial technologies for two reasons. First, there are many regulations that help maintain the US dollar as the vehicular currency, used by central banks and other financial institutions to secure assets. Second, many developers of the technology are hesitant to throw it upon us – yet.

But this will change as the robustness and reliability of cryptocurrencies is proved study by study and case by case. One method is by using cryptology.

Cryptology is used to protect your information from hackers. In fact, the protection of your data is more important than ever before. We have made our lives more public thanks to social media.

While you may not mind so much if hackers get unauthorized access to your pictures and social media profiles, some information is actually valuable. This includes your banking details, birth certificate, licenses, and intellectual property.

The Covid-19 pandemic has forced us all to work from home. Those employees of numerous companies are accessing commercial information using personal computers instead of office computers. But personal computers might lack anti-virus software, firewalls, and other security measures.

Right now, cybercrime is costing companies at least $45bn a year worldwide.

This is why now is cryptology’s time to shine. It will also be used to protect your online purchases made using cryptocurrencies instead of traditional money. It will help ensure that funds go from your bank account to a retailer’s quickly but securely.

Using Crypto for daily activities

Let’s face it, we are going to use Blockchain for shopping: Lamborghini already accepts purchases in Bitcoin. The concept might still be difficult for you to grasp, but they are still being developed and soon it will be near impossible to live without them.

Gaming companies are already embracing cryptocurrencies. Fortnite, a popular online game, with more than 250-million players, allows you to buy in-game products using cryptocurrencies.

Beyond regular shopping, you could soon buy a house using a cryptocurrency. Blockchain technology and the underlying distributed ledger technology is being used to increase transparency in real estate transactions using smart contracts.

To reiterate the use case for Crypto, many countries like Germany are relaxing laws and giving licenses to allow ‘Crypto Banks’ to operate. This is one effort to ensure that your Cryptos are properly taxed when used for investment purposes.

One such bank, Bitwala, allows you to purchase Bitcoins or Etheruem securely and quickly from a charges-free bank account which they provide.

Your transactions are then documented so that you can seamlessly submit reports of the purchases to the local tax authorities (Finazamt) to avoid penalties. You can do this all directly from the Bitwala App.

The blockchain and cryptocurrency are even being explored on national levels: China is allegedly creating its own national digital currency.

The way forward

Monetary systems will continue to be tested every day. Banks the world over are spending big bucks to protect themselves from hacks. But one day, a hacker could throw them into turmoil.

When that happens, you might be unable to withdraw your money. A central bank’s database could be hacked making it difficult for it to work with other banks. In the meantime, alternatives to classic monetary systems need to be developed.

Cryptocurrencies backed by cryptology could be a very strong alternative. There are also some valid cases for using Bitcoin as a global currency. This, however, will only become a reality if it shakes off its high trading volatility to become more stable.

We live in a world where we need to be cognisant of our health and how viruses can spread easily and quickly like wildfire. It equally is imperative to realize that cyber attackers could get and infect our data just as swiftly. Using modern technologies can help prevent these intruders from creating a ‘digital security collapse’ pandemic.

Did you know that there are still more than 700 million people in the world who live in extreme poverty? These people must scrimp, starve, and struggle to survive off less than $1.90 per day.

By 2030, the World Bank estimates that more than 90 percent of those people will be concentrated in Sub-Saharan Africa.

This is perhaps one of the greatest developmental failures of the modern world. Despite the continent’s expansive natural resources and increasing connectivity, foreign actors still feel it’s too risky to heavily invest in their markets.

Blockchain could be the key!

Bitcoin and “Blockchain” were created in the mass wave of distrust in banks after the 2008 financial crisis. Therefore, the technology enables individual, distributed data storage that could become the perfect evidence (trust) base and financial infrastructure for a developing country.

With the right implementation, Blockchain holds the potential to completely revolutionize and revitalize such economies, especially in Sub-Saharan Africa.

So, what is this Blockchain?

Blockchain is essentially a kind of decentralized database that allows you to have a safe, secure way to handle their data without the need for third parties.

For example, you could with Bitcoin, make or accept payments in real-time without needing a centralized bank.

“[It is] a way for one Internet user to transfer a unique piece of digital property to another Internet user, such that the transfer is guaranteed to be safe and secure, everyone knows that the transfer has taken place, and nobody can challenge the legitimacy of the transfer,” said software entrepreneur Marc Andreessen.

“The consequences of this breakthrough are hard to overstate.”

Historic background

Until the mid-twentieth century, most of Africa was ruled under a colonial system meant to exploit the people and their natural resources for European benefit. Africans, in addition, were rushed into development according to European standards rather than homegrown ones.

The legacy of rapid development, distrust and corruption left behind an economic system failing to recover in the 21st century.

While the World Bank celebrates a decrease in global poverty levels, the number is expected to remain stagnant in Africa. Today’s poorest people are living in places with the least economic growth.

Sadly enough, poverty and lack of investment in many developing countries stem from how they were integrated into the world system.

The land was cut into countries according to European treaties and agreements, rather than by traditional and tribal land divisions. This situation worsened upon the handover of colonial power to so-called “democracies.” Power often shifted to the ethnic groups that former colonizers favoured.

Corruption multiplied in the form of bribes, political persecution, rigged elections, and a massive wealth gap. All of this still affects the wealth distribution and investment potentials of many developing countries.

Of course, this created a lack of trust in banks and government throughout much of Sub-Saharan Africa.

The perfect fit for Africa

During a 2012 study conducted in rural Western Kenya, Stanford University researchers waived the costs of opening basic savings accounts for a number of unbanked individuals.

While 63 percent of the subjects opened an account, only 18 percent of them used the accounts. This was likely due to three factors: a lack of trust in banks, unreliable service and prohibitive withdrawal fees.

Unfortunately, the prevalence of unbanked individuals in the informal sectors scares off foreign investors, who heavily rely on transactional evidence to make investments. Otherwise, pouring money into markets is too risky. That’s where Blockchain comes in.

How would it work?

Blockchain can host an entire evidence base of transactions, loan repayments, and asset titles. The technology is also decentralized and requires individual confirmation, creating an element of trust and transparency beyond traditional banking systems.

According to Victor Olorunfemi, Director of Products for Pan-African tech and crypto-exchange, KuBitX, Blockchain’s major benefits lie in “frictionless P2P and cross-border payments, transparent elections, land registry management [and] transparent crowdfunding.”

Let’s look at some of the different ways Blockchain could benefit developing economies, especially in Sub-Saharan Africa.

1. Creating financial infrastructure and accountability

According to a study by the Milken Institute, viable financial markets require consistent, accurate data on assets and credit histories. Luckily, Blockchain may fulfil these needs.

The use of Smart Contracts technology is ideal in areas lacking accountability, such as the real estate or land/agricultural sectors. In Africa, a lack of record-keeping practices often leads to “missing” or non-existent title deeds. In some cases, this is intentional.

Title deeds “go missing,” only to end up in the hands of benefactors other than the rightful owners. Smart Contracts could eradicate these issues through the use of special tokens that cannot be duplicated, changed or removed. See the article on tokenization.

Likewise, Bitland, a company in Ghana, currently helps individuals record deeds and land surveys. By resolving land disputes, Bitland creates more stability while accurately recording land asset data.

“There’s a massive number of people in the informal sector, but there’s not much data being collected on them right now.”

Merit Webster, co-president of the MIT Sloan Africa Business Club.

“That means you don’t have that credit history or payment history for them. If you have a decentralized approach to collecting data, you end up with more malleable data. [This] is very valuable for creating credit histories.” The agricultural industry also has the potential to thrive using Blockchain.

“Blockchain could be used to track goods around the world. This allows farmers to earn a fair wage for their goods.”

Also, farmers could use record-keeping technology to streamline the supply chain and document resources. This would lead to better efficiency, lower transactional costs, and improved logistics.

2. Security in banking

According to the World Bank, there were 1.7 billion people with no bank account in 2017. This situation is worst in developing countries, especially African ones. For example, over 62 million of these people lived in Nigeria.

Besides, data from Google Trends reveal that Lagos, one of Nigeria’s biggest cities, ranks globally as the number one city based on the volume of online searches for Bitcoin (BTC). Clearly, for the city’s 21 million-odd people, there an immense interest in some form of an accessible payment system.

Of course, it’s unrealistic to expect bank branches to magically appear in every remote corner of the world. However, a digital database using Blockchain technologies has the potential to reach far beyond physical banks.

Ad: N26 Bank

Many Africans value trust and transparency. In developing countries, this lack of trust goes beyond the Internet. Developing countries with less industrialization tend to have higher levels of corruption.

This reduces national investment opportunities in the public sector and instills a lack of trust in centralized oligarchs handling an international investment.

Because its power lies within the community of users, Blockchain can combat these trust issues. All data logs and amendments must pass through this community and identification confirmation tests.

Blockchain technology also secures your data incredibly. Hacking and data breaches are all too common nowadays. In 2017, for example, around 3 billion Yahoo user accounts were stolen.

When information is stored in the same place, hackers have one, easy target. In contrast, Blockchain is a distributed entity. This dissemination of data leaves it far less vulnerable to cyberattacks.

3. Fostering Entrepreneurship

Coupled with the Internet, Blockchain technology could be the perfect platform for aspiring African developers. Because the ‘source code’ is free of charge, skilled coders can adapt, create, and configure special applications, called DApps.

These are available on Crypto platforms and provided by companies like Ethereum, and a South African firm specializing in what they called the Keto-Coin.

Rather than waiting for governments to drag their feet trying to create jobs—individuals on the continent can form small firms that build and sell Crypto-based Apps locally or abroad.

“Despite the frictions and impediments mentioned,” said Olorunfemi. “Blockchain can still provide an avenue for promising African tech projects to access capital (FDI) via token offerings on digital assets exchanges.”

Many courses are even readily available online to quickly learn about new technology. Microsoft, for instance, offers a platform via Azure for you to build and learn about the Blockchain.

One-man shops in countries with unfavourable economic systems, like Zimbabwe, can also adopt smaller, stable, Cryptocurrencies to facilitate or payments. In cases of rampant inflation, they can temporarily act as a store of value or help you pay for things until your currency stabilizes.

As with the Venezuelan hyperinflation case study, Cryptocurrency intervention could help many developing countries troubled with economic instability.

There is also the option of Crypto-mining. But before you pull out the ‘high-consumption energy’ argument – think outside the box for a moment. What about energy sources that are free and available nearly 24/7? Like water and the sun!

The African continent is full of capable scientists and mechanical engineers. One could build special solar-powered energy centers to power Bitcoin-mining.

And without the expertise, governments or private companies could alternatively just invite Crypto companies with abundant financial resources to mine (cleanly) for a special tax/fee while creating jobs for the locals.

4. Elections

In addition to the financial side of things, Blockchain technology could help eliminate some forms of corruption. For example, many African countries’ elections are incredibly vulnerable to the social scourge. In some extreme cases, some officials change or forge written ballot votes to rig elections.

To combat this, Blockchain databases could record votes. This makes it nearly impossible to tamper with using Smart Contract technology. Having fair elections improves infrastructure, which then increases development and economic dependability.

While some might see Africa’s economy as underdeveloped, others might see it as a blank canvas well-suited for a large-scale implementation of Blockchain. Economic and governmental systems are shifting and slightly shaky in many Sub-Saharan African nations.

The challenge is to foster a rigid economic system to implement Blockchain.

Don’t just take our word for it—African nations have often implemented new, practical technologies before the Western world. Let’s look at the example of M-Pesa. Back in 2014, Americans and Europeans were amazed by Apple Pay’s launch.

However, this mobile payment system wasn’t exactly “new.” By that time, Kenyans had used M-Pesa, a very similar technology, for years.

“There’s a lot of opportunity to leapfrog the way the West developed and have these more unique African solutions, but it needs to come from within,” said Webster.

“It needs to come from entrepreneurs in the continent who want to implement these solutions. It’s important to engage people very early on. Systems incubated in the West don’t stand as great of a chance to work as African ones do.”

Concluding remarks

With the possibility of an experimental, large-scale takeover of Blockchain technology to improve African infrastructure, the nations there could leapfrog in development and growth.

This must begin internally. According to Olorunfemi, “Education—of policymakers and other stakeholders—which is often ignored has to be a critical factor in paving the way for the acceptance and adoption of new technologies and the accompanying investment.”

The results in Sub-Saharan African countries could help eliminate much of the world’s poverty. It would also remove remnants of mistrust and corruption left behind by the days of colonial exploitation.

While there are some obstacles to large-scale Blockchain implementation, we can’t think of a better benefactor than there. The possibilities for business using the Blockchain are endless!

To learn more about how to get started with Cryptocurrency mining or purchasing, visit our resources page for useful links and guides.

Additional input by Bobby Quarshie (BQ).

Citations: Christopher Lee and Jackson Mueller.

Swan, Melanie. “Anticipating the Economic Benefits of Blockchain.” Technology Innovation Management Review 7.10. Oct. 2017.

Bitcoin Lessons from Venezuela, Where Hyperinflation Reigns. Online Source: https://www.lathropgage.com/newsletter-237.html

When considering small business financing, it is important to understand all your available options. If not, investors can easily take advantage of you and offer unfair terms.

So before raising any money, find out if using equity, debt, or convertible debt financing makes the most sense for you to grow your business.

Equity

Raising capital through equity is popular, if not the most popular choice, for entrepreneurs to pursue. Investors buy stock (or shares) in your company, giving them a financial stake in the future success of your business.

How It Works:

You set a specific Dollar/Euro amount for what your company is worth.

Based on that valuation, investors agree to give you money in exchange for a certain percentage of your company.

Investors receive compensation based on the percent of stock/share they own once you sell the company or go public.

Pros:

All your cash can go toward your business rather than loan repayments.

Investors take on some risk and don’t have to be paid back until you’re doing well.

Investors often have valuable business experience.

Since investors have a financial stake in the success of your business, they are motivated to offer sound guidance and valuable business connections.

Selling shares of your company will make it very difficult to get them back.

You will also most likely lose control of part of your board to your investors.

Debt

Debt-based fundraising is the form of small business financing that most small businesses end up choosing, according to Fundable. It is also the easiest to understand. Money is loaned to you with the agreement you’ll repay it over time with an established interest rate.

Get a quick loan for your business here:

How It Works:

You borrow money with an agreement to pay it back with interest within a specific time frame.

You will also have to offer your lender some form of collateral, which are liquid assets you will give up if you cannot make your loan payments.

Pros:

You will raise capital much quicker than with equity small business financing. This is especially true of smaller cash amounts.

You can keep 100 percent ownership of your company, along with 100 percent of its profits.

Interest payments are tax-deductible.

Cons:

You must be completely confident you can make your loan payments in cash each month. If you don’t, lenders can make you sell your business in order to get their money back.

Interest payments can become one of your largest business expenses.

Commercial lenders will demand small business owners to personally guarantee the loan and offer personal assets as collateral. This even if your company is structured as a corporation or limited liability company, according to Forbes.

Convertible Debt

A convertible debt small business financing structure is a mix of debt and equity financing. The money raised is considered a loan, but at some future date, the loan can convert to equity if the lenders so choose.

How It Works:

You will negotiate an interest rate to pay back the loan. This will also be the interest rate for those lenders who decide not to convert any debt into stock.

The details concerning how lenders can convert the debt into equity are negotiated at the time of the loan. For the most part, that means agreeing to give lenders a discount or warrant on an upcoming round of equity fundraising.

You will also set the valuation cap, or maximum company valuation, at which lenders can convert debt into equity. If investors decide not to trade in their loan for shares at this predetermined valuation level, they can no longer do so at a future date.

Pros:

Transaction costs are low and the process moves quickly.

If you don’t want to set a company valuation, which involves a lot of uncertainty and risks for new startups, a convertible debt structure for small business financing makes a lot of sense, according to Covestor CEO Asheesh Advani.

Using convertible debt protects investors from dilution in future financing rounds.

Cons:

Investors are uneasy about giving money without knowing the exact share of a company they will own. You might have to offer steep discounts on equity in order to get them to agree to the terms.

You may be forced to set a valuation before you are ready in order to avoid unaffordable loan repayment expenses.

In the end, it’s best you make your final choice, based on which of the mentioned options works best for you, not just now, but in the immediate future.

UpCounsel is an interactive online service that makes it faster and easier for businesses to find and hire legal help solely based on their preferences.

In economic terminology, the term “utility” has not much to do with multifunctionality nor completing specific useful tasks.

It does in context, relate to the level of satisfaction or “completeness” one derives from the consumption of a product or service. For example, there is only so much pizza you can eat before feeling ill from satiety.

On a broader and more macroeconomics spectrum, our utility levels will also help determine how resources are allocated and consumed.

Definition

The concept, a brainchild of Daniel Bernoulli, has so many relevant connotations. As humans, we individually have a maximum biological boundary which when reached, signals absolute satisfaction. This in economic terms is called maximum (total) utility.

Total utility is the complete satisfaction that you can get from consuming all units of a specific item.

Economists are more interested in the changes in levels of utility or what is referred to as the marginal utility.

We will return to its application to the economy.

Applying utility

Incidentally, the utility has no formal unit of measurement – though we coined the term “utils”. These so-called utils equate a number to utility levels in a controlled sample experiment.

Understandably it can be quite a feat to quantify utility as it is based on human behavioural preferences. The closest we got to quantifying such was via the marketing concept of the consumer black box.

As an illustration, the concept can be applied to something as basic as eating a delicious meal.

Depending on how hungry you were, you would derive the highest utility from the first few bites of your meal.

As you progressed and depending on your appetite, each additional fork/ spoon, or handful would provide fewer levels of satisfaction. As you reach your stomach’s capacity (towards satiety) your utility diminishes.

This can be applied to the taste of the meal. It specifically explains why we tend to eat something sweet after a main (savoury) meal.

The appreciation of ice cream when you are starving would diminish quickly as you concentrate on filling up your stomach. This as opposed to enjoying the taste.

When compared to the running of an economy, governments and policymakers can determine which goods and services yield the most utility.

This helps them to consequently direct expenditure to identified priority areas (products/services).

It is a long term concept

Education, for instance, may not provide immediate utility (gratification) for scholars and pupils. However, when appropriately harnessed, could yield higher levels of satisfaction. This is when you enter the job market with better remuneration packages.

Tweaking education curricula, taking into consideration levels of utility to whip up your interest for the good or service. This should, therefore, be a prime focus for legislators.

Inputs such as maximum times you can concentrate and the length of study for a course should be offered without compromising the substance.

Without a doubt, there would be considerations, at a micro-level to assist in enhancing both marginal and total utility in the education sector.

The concept of utility is a lot less ubiquitous as we think and relates to the unsavoury phenomenon of megalomania and why there is greed. When levels of self-gratification diminish quickly, it takes longer for those with lower levels of marginal utility to reach a plateau of pleasure.

Drug addiction, sexual appetites, and fetishes would then kick-in. In such cases, people upgrade the “product or service” that they have already maximized utility in. At that stage, another level of fulfillment would be sought.

The utility applied to finances

It also explains why you lose a lot of money gambling or investing in stocks. The satisfaction of gaining more for a little outlay will often drive you to take more risk until a level of risk aversion kicks in.

High-risk investors “called whales” are now delving into the Crypto market to maximize their utility. They are diverting their funds from property and stocks into digital currencies like Bitcoin and Ethereum.

The saying too much of a good thing is inevitably bad for you applies. It can be countered by diversifying the things that deliver pleasure or satisfaction to you.

This is to ensure that you do not maximize utility on them too quickly and lose interest. Worse case, you end up delving into the dangerous territories of addiction.

Economists need to be relevant, more than ever before. They also need to formulate a means to measure and quantify utility or provide “utils” for at least, the most common goods and services.

With such a strategy, policy-making, product pricing, and the efficient allocation of resources would be more effortless.

As an Arsenal Football Club fan, one has the natural tendency to follow the progress of both present and past players of the revered North London title-winning institution.

The prestige of playing for the club comes along with all the bell and whistles required to make life living in the small yet expensive hub city often dubbed to be the centre of modern Europe, a breeze.

It was rather sad to read about the unfortunate fortune of a former player who had a big heart and passion for the beautiful game. He was, however, a bit aloof and care-free on the pitch. It turns out this was a character trait that perhaps extended to his financial affairs.

He was recently reported as sleeping on the couch of a friend without a penny to his name. How can that happen, you might ask?

His weekly wages were a reported 50 000 Great Britain Pounds! So how did he go from earning that figure, to being dead broke?

Such a bad turn of fortune is not uncommon for celebrities, qualified professionals, and lottery winners. This can be explained by a simple lack of ‘investor mentality’.

The right state of mind

This mindset can be instilled in us from a relatively young age if you have had the luxury of growing up with parents, teachers or a mentor who imparts this knowledge to you. It can also be learned later in life – often the hard way.

Similar to starting a business, the biggest barrier to entry into any form of investment is always the initial capital. Once you have it, coupled with the investor mentality, it’s hard to fail financially in life: just ask the current sitting American president!

Now as obvious as this sounds, you need to put in money to make money. That is why investing, for instance, is mainly carried out on a large scale by banks – with your money!

What you do with the money when you inherit it, win it, or save up from a weekly or monthly project-based income is more important than just having it in the first place.

Wouldn’t you agree that money comes then often goes faster than you realize? Having a grasp on why it leaves so fast is what we should be paying attention to.

Let’s firstly be sensible about this – investing is always a long-term project. A desire to reap short-term gains or having such a mentality is paramount to risky gambling or betting against the odds.

“Patience is an investor’s game – if you don’t have any, don’t bother with the mechanisms that don’t lock you in for a few months to enable you to realize a return.”

Enough of the rhetorical questions and statements. Let’s briefly look at a few investment vehicles in the true fashion of Debunqed.

Savings

This is the least risky investing vehicle and tends to suit patient investors. Usually, it is for you if yo are the kind that loves to watch paint dry. 🙂

Your only risk would be using a non-government backed bank for it. The higher the amount you invest, the better the interest rate you get. So this basically benefits the already wealthy. Some savings accounts are even known to offer you 0% or fractional decimal interest rates which are calculated nominally.

So it begs the question – why would you even consider putting your money in savings? Well, using this investment strategy helps with a good credit score. That comes in handy when you apply for loans or obtaining financial backing to start your new business. So they do have some use. Risk level: Little to none.

Property(residential or commercial)

This is the golden nest egg of investing – that is if you can raise the bond for property or inherit one.

Property is one asset class that tends to only appreciate and relatively well over the years depending on what is happening in the area/town or economy. Getting in is the difference between having a spender or an investor’s mentality.

What do we mean by this? Well, if you can save up for a deposit to buy a brand-new luxury car, you could and should do the same for a house.

That way each “monthly rent” payment goes towards something you will eventually own. You could also buy-to-rent. The income generated from the tenant (rent) will help you pay off the bond.

Consider the appreciation value of property in your local area over the years. But like anything valuable, you must be prepared to maintain its upkeep – the costs will be more than your weekly carwash.

In the long-run when you realize the greater future value, you could even downgrade to have some extra cash to spend. You could then get that car of your dreams or travel and see the world. Risk level: Low to moderate.

There are a number of online trading platforms out there so it is a good idea to go with the accredited ones.

One of the key benefits is that they all offer a free trial – which often gives you a mock .account. That’s a great way to learn about the tools and the above-mentioned markets.

There are aspects you need to pay attention to. One of them is leverage trading . It is essentially borrowing money to trade (payable with interest) – a double whammy if or when things go south for you. Risk level: High to Excessive.

Mutual funds

As the name suggests it is derived from a pool of funds from a specific institution or industry. Mutual funds are offered by institutions as a supplement to retirement plans (pensions and annuities).

They offer you a return (often a stable monthly or quarterly pay-out) based on a fixed term that you agree on with your portfolio manager. The offering institution would then apply your pooled monthly contributions into a diverse portfolio to spread your risk exposure.

This, however, requires the attention of a (paid) portfolio manager and is thus susceptible to the principal-agent problem. Risk level: Low to moderate.

Venture Capitalism/Angel funds

If you have some spare cash and don’t want to bear the risk and burden of running a business yourself, you can fund other people you believe will be successful.

In this arrangement, confidence is placed by you on the owner and the offering. You can then state the terms for the release of your funds such as a quarterly return on investment or a larger stake in the business and its profits.

Rapper Nas is known for his investment in Silicon Valley start-ups as a Venture Capitalist – which gives him a share in the companies he backs with the hope of it growing exponentially to increase that shareholding’s worth.

Celebrities and sports stars usually have the capital to diversify their portfolio by investing in or starting up a new business. One such notable venture was the one where Rapper/Producer Dre’s Beats brand got bought by Apple for three billion USD. Risk level: Moderate to high.

Rare items

Though not an easy commodity to come by because often the initial value can be quite high (unless of course, you are lucky to find an item at a junk sale or low-key auction), rare commodities can also form part of your future financial security.

Rare coins tend to take a long time to mature in value. Likewise, a painting can appreciate quickly in value if the artist’s “interesting” background comes to light in the press for good or bad reasons.

As an example, a rare Nelson Mandela coin once sold for 100 000 USD while he was still living. So, one can only imagine what the few in circulation are worth now.

A rummage around old antique shops and secondhand sales can reap rewards if you know what you’re looking for. Risk level: Low to moderate.

Bonds

These are long-term interest-bearing certificates issued primarily by governments (via monetary policy) but also by certain large public institutions.

Bonds give you a guarantee of a future value using a specially controlled interest rate. They are usually issued with fixed terms and can only be accessed after 3 to 10 years.

This locks you in, to hold the bond for the agreed period regardless of which way the interest rates are going.

Naturally the higher the rates the better for you. As a cautionary note, you will be subjected to the regulatory activities and monetary policies of the country in which you hold the bonds. Choose where you buy very wisely. and research your product.

Accessing bond markets is also not easy and you may be subject to complex rules pertaining to the country, residence status and your credit score, and so on.

It is really for the long-term investor and can be used in the same way mutual funds tend to be applied, to supplement one’s retirement annuity package. Risk level: Moderate to high.

All things investment

You need to remember the importance of imparting this knowledge to our youth, friends, and family so as to continue the cycle.

The simple answer being: Education. The lack of it is one of the fundamental causes of poverty.

A number of celebrities and sports stars have overlooked it’s true importance so as to follow their true passion and skill. This is not necessarily a bad thing. If you have the right people around you to help you manage your finances.

It was reported he signed documents without knowing the full content and liability of what was being presented to him. It was also said that she would even bring paperwork to the football club’s training ground for him to sign.

Let’s be honest, we don’t know the full facts but there is a lesson. This “wife” character could be anyone that you entrust with managing your finances so, be wise as to who you choose to oversee your accounts.

Make a plan

Having a grasp of your assets (if any) less your liabilities is the first place to start. Once you know what you have or don’t have, you can then set goals. Think about what you need to do to achieve a net worth that will sustain you for the long term.

Granted we all must pay bills. We will write down that part of our income but we need to focus on what is being done with the money that is left once your overheads are met.

Educate yourself (skip a binge session on Netflix). Take a deeper dive into the investment vehicles briefly spoken about. The resources page will provide more comprehensive details about all seven vehicles discussed.

It will also guide you on where to go to find out more once you have decided and which vehicle or combo would fit your investment type and appetite for risk.

Make 2018 a sensible year finance-wise and happy investing!

The implementation of globalization has not been without its major flaws. Abolishing it, however, is paramount to anti-socialist behaviour or looking inwards. This concept is against the tendencies of human nature.

If you read up on any definition of globalization, you will see that the intention was always genuine. The need to integrate and collaborate for the mutual benefit of nations.

It can, however, like any product (like knowledge), be exploited out of selfish desires and lead to exploitation.

Of course, it also doesn’t mean that globalization must apply to every sector of your economy. Some inward investment is always healthy. It should, however, not lead to extreme nationalism for a fear of loss of national identity.

Trust issues

The problem, like many others, lies in the hands of politicians who are controlled and dictated to by a handful of large corporations. These ‘corps’ have one and only self-interest – profit, power, and control.

The main concern for sovereign governments is that ‘giving up’ or sharing one’s technological, innovative, or manufacturing secrets to other countries. The premise is that this would make them ‘vulnerable’.

The real issue lies in a lack of trust – leading to the notion: “I will not let you know how I do it because you may use it against me – in trade or war”.

Despite the existence of supposedly ‘compartmentalized’ trading blocs and free trade areas like NAFTA, EU, ECOWAS, SADC,etc, the rate of globalization has sped up significantly in the past decade.

This is due to boundless advances in information technology as accurately predicted by Neoclassical Growth Theory.

Information technology has now given us valuable new tools to identify and engage in economic activity.

Tech provides access to and faster, more informed analysis of information, transfers of assets, and collaboration.

The impact on finance

A globalized world means that with the aid of technology, you can buy and sell shares of an Italian firm from a desktop in Namibia!

You would then only have to deal with the commissions and transaction fees (capital gains tax) locally pertaining to your online trades.

And think about it, on a micro-level. If globalization is entirely a bad concept then no-one should be using Amazon, eating MacDonalds, or watching Netflix in protest. Hard to imagine, isn’t it?

We must praise its positive outcomes and work hard against the negative impacts. The negative ones are also giving rise to a new era of extreme nationalism or populism.

You can only do your bit by promoting and backing policy-makers who can enforce good trade laws. This would force both local and international competitors to play by the same rules.

Penalties for financial misconduct should be a lot greater to deter exploitation. Rather, perpetrators still get the proverbial slap on the wrist.

The creative destruction of the financial system will be brought about by cryptocurrency and its underlying blockchain technology.

Depending on its uptake, and whether the authorities can legitimize its legality, we may see individuals and governments using decentralized currencies.

The Venezuelan president is investigating the concept of a national cryptocurrency dubbed ´Petro´. They would use it to alleviate dependency on (heavily interest-ridden) loans.

When it comes to providing means of storing, sending, and receiving money, banks and their affiliated institutions, have enjoyed a monopoly for centuries.

They (especially central banks which allegedly are owned powerful families) have the authority to influence countries and their governments. We will not go into the level of control as this paves the way for conspiracy theories which though not proven – are not farfetched.

So, it’s only expected that when some new and unknown entity threatens their prosperity, they start to react.

Blockchain frenzy

How banks are responding is evident by how they are fervently building their own blockchains. This, however, defeats the purpose of a having decentralized system.

Bitcoin and cryptocurrencies get their appeal not just because they are very secure. But because unlike fiat money, they are not heavily regulated and can be mathematically restricted.

The 21 million unit limit on Bitcoin by default places it closer to the status of gold (which is also not infinite). But what happens when all are mined in 2041? Bitcoin’s current ‘value’ of over $30 000 (adjusted),could move up again, according to the traditional laws of supply and demand as it becomes rare.

To unlock more value the creators will split it again. The first major splits (forks) gave rise to Litecoin and Bitcoin Cash. Both cryptocurrencies are racing to newer heights daily.

How banks operate

Now back to the banks – they make money from our deposits and these deposits are backed up by our reserve banks. Reserve banks lend retail banks money which they essentially just print. The banks must ‘turn it’ and pay it back with interest (repo rate).

So, technically we ‘empower’ banks by depositing our money so they can invest the funds in all sorts of mechanisms. Such mechanisms include the credit and loans to you, your businesses, equities, and property.

Then, they also invest in high-risk investment vehicles like currency trading, derivatives (futures). They are essentially the biggest regulated and legal Ponzi-schemes. They also make a significant amount of the daily fees they charge you.

A quick example

Let’s quickly put things into context. A bank with over a million customers transacting daily. Let’s say they charge you a 10 cent (conservative figure) transaction fee for depositing, withdrawing from another bank, or an intra-bank transfer.

They then make 0.10c x 1 000 000 = 100 000 units of the currency on the day. This equates to 1,2 million Euros, Dollars, Rands, or Yen annually. And that is just off your transactional fees!

Then they also charge you monthly service/maintenance fees. Those are to cover the convenience of you having an account and, for services like online banking.

This is what cryptocurrencies can potentially wipe away from banks we all go the digital currencies route. Granted, how you acquire and transfer Cryptocurrencies are not as straightforward as receiving paper money – yet.

That, coupled with the stigma around ‘Cryptos’, means there is still a barrier to entry for the ‘open-source’ monetary system.

Banks will try and bring about their own blockchains to address security concerns around making transactions. For them, however, it would still be business as usual when it comes to the charges.

Birth of Fintech

Some newer financial institutions, however, are already progressing in the favour of you and me – one such is the European based N26 Bank.

We often end up paying for things all month without even having to go to an ATM. It works as a traditional bank would, however, allows the (smart) card to be used as a credit card (backed by Mastercard) would.

This allows you to quickly purchase goods online, book events, flights ticket, and accommodation. Basically, all things you still can’t do with your debit card.

In countries like Sweden and Estonia, card and digital systems have been a thing for a long time now.

Some of these Fintechs are adopting or partnering with Cryptos companies to deliver their services. One such as the relationship the one between a German bank and the crypto Ripple.

Click image topurchaseRipple here

It would be interesting to see what governments and financial institutions do to ‘protect’ their payment systems. Likewise, it will be equally fascinating to observe how they adapt in general to the new digital era upon us.

Warren Buffett once referred to financial derivatives as “weapons of mass destruction” . He warned that they are detrimental to the global economy and financial markets.

Cryptos have a way of creating something supposedly of intrinsic value out of nothing. This is as dangerous as propaganda that leads to conflict or promotes struggle.

They are backed up by a cloud of non-regulatory policies by states who themselves, still traditional monetary policy measures.

And this is despite their full understanding of the instruments of financial wizardry.

In economics, the term creative destruction, however, has a paradoxically positive meaning. It is perfectly suited to the new form of “crypto”- currency (Bitcoin) that is not as mystic as it seems.

A brief history

Money is a concept that probably also met up with resilience when it was first supposedly introduced by the Chinese. They started carrying folding money during the Tang Dynasty (A.D. 618-907).

The instability generated by uncontrolled usage and denomination, however, soon led to rapid inflation. This prompted the Chinese to drop it, only for it to be taken up again later when it got stabilized by the adoption and use by the West.

They developed paper money as an offshoot of the invention of block printing. Block printing is like stamping.

Ironically that very same term ‘block’ is the foundation behind the Bitcoin – which is generated using blockchains (digital public ledger).

We won’t get into the mechanics of Bitcoins. We will, however, attempt to increase awareness on why and how this new payment method could cause positive ripples in the financial global system.

What is Bitcoin?

As per Wikipedia, and as simple as it can get in terms of a description: Bitcoin is a cryptocurrency and a digital payment system.

It was supposedly invented by an unknown programmer, or a group of programmers, under the alias Satoshi Nakamoto in 2009.

Though the anonymity creates an element of distrust about the agenda of its creators, it is surprisingly more transparent than derivatives.

Cryptocurrency uses a system of cryptography (encryption) to control the creation of digital ‘coins’ and to verify millions of transactions.

These transactions include are a basic movement of funds between two digital wallets and get submitted to a public ledger and await confirmation through encryption.

This video is a great and simple way for you to understand the above because it is best understood when explained as a larger picture. Check out this useful and basic video on Bitcoins.

That is quite a feat worth acknowledging because 11 years of existence is nothing compared to gold’s multiple century reigns.

Now 2009 was not long ago considering the Bitcoin is now ‘worth’ well over $20 000 each (updated to 2021 levels).

For centuries, gold has been our standard of trade or backing of all types of currency until it was ‘uncoupled’ by Nixon in 1971.

The future of trade and commerce is in the digital sphere – are you in the know?

Potential currency?

For something to become the standard measure or mode of trade it, however, needs to be stable. So, while the technology behind Bitcoin (the Blockchain) is relatively sound, its actual price needs to find its firm nesting.

Established currencies trade on markets via exchange rates with relatively minuscule increments of change in price and value. In comparison, Bitcoin can jump in value by $1000 within (minutes or seconds) – prompting skepticism about its stability.

Google Engineer Ray Kurzweil, who is revered as a “prophet” for his mysterious predictions, such inconsistency undermines the cryptocurrency’s value as a currency.

The aim is nevertheless to relieve our dependency on money or more so, the iron grip and often abusive control that some banking institutions have over consumers.

You could even argue that the recent surge in its price is being fuelled by agents of the traditional banking industry. They naturally feel threatened by the fact that they may not fully understand it and its inherent potential. So they (cash-flush) could inflate it for an inevitable ‘burst’.

But the currency though very volatile in its movement has remained buoyant. It has now held for well above $10 000 for sustained periods since its inception. Gold is now approx. $1,900.

Bitcoins provide more guarantee than financial derivatives especially because of their open-source approach to its existence and use.

Complexity

The tricky part is simply getting to grips with the vastly abundant information about it and how you could even generate it.

It is still a great backup ‘of a backup’. We rely on technology and more specifically the Internet for transactions and the associated traffic for our daily lives.

A simultaneous crash of a few major servers, however, could send it all tumbling back into the digital abyss. But as with money and other forms of currencies, only time will tell.

Bitcoin will just have to further prove its resilience and stability in the long run.

Getting attention

It is certainly not a ‘fly by night’ thing because it has sparked the interests of both public and private institutions globally. China even made a bold move to block the Bitcoin market from trading within its borders at some stage.

Bitcoin also gets its collective strength (intrinsic value) from its limited quantity in circulation (19 million out of a finite 21 million).

Spillover effects

Bitcoin has also paved the way for others such as Ethereum, (mostly used for smart contracts and by developers) which is also seeing good growth. Then there is Litecoin, which was formed as part of a controversial yet civil split from the originators of Bitcoin to use ‘variant technologies’.

All these platforms (companies) now use the blockchain to create all types of cryptocurrencies to capitalize on the spoils of this digital revolution.

There are also several institutions that are offering late-comers a chance to benefit from the spoils of using and investing in digital currency.

Naturally, all these schemes with their investment packages would require a ‘buy-in’ and marketing to attract more takers.

Such Crypto ‘companies’ are likened to a pyramid scheme and subject to many investigations by fiscal and criminal authorities. But that is how Bitcoin, its promoters, and the market were initially treated.

Interested? Check out the following useful links to their official websites to help you get started.