In a few years from now, cash may no longer exist. Instead, we might be using microchips in our hands which will communicate with a digital currency system. As humans, we want things (and processes) to become more uncomplicated. That is how we measure progress.

Right now, technology facilitates economic activity but may soon supersede the need for faulty monetary policies (by creating more efficient economies) in the long run. Robert Solow was right all along. Despite this, we still use archaic paper currencies. This form of legal tender, however, in a decade or sooner, might be replaced by another official means of exchange of many nations – or at least be in heavy use.

Society needs a safer, easy-to-use means of exchange and incidentally, as you read this, digital currencies are being designed and studied at Universities and information technology ‘thinktank’ companies the world over.

It would require a monumental shift in thinking for people to stop using cash at all. At a human level, it seems simple. Paper money is (literally and figuratively speaking), dirty and it takes up space. It’s also possible for cash to cause stress as when you have it – you have a target on your back.

So, what could replace cash?

Central Bank Digital Currencies (CBDCs) are currently in hypothetical planning stages with some countries conducting proof of concept programmes. CBDCs are a means of monetary exchange (by a Central Bank) that exist in a digital state on a server in a cloud.

The idea of using a CBDC was prompted by the emergence and prevalence of Bitcoin and other cryptocurrencies. Believers in the mass use of CBDCs want the world to use less cash. They believe people are safer if they do not have money at hand, which can be stolen, and that commerce can be more efficient in a cashless society.

We could say that the history of money is a story of its gradual dematerialization from tangible objects to intangible computer code. Programming code is written for and used to facilitate many facets of our lives, so why not with money?

An ETA is sooner than you think

Over time, what has been used as money has changed, starting from trading large objects which were seen as a basic store of value. Gradually people started shrinking those objects into paper and then turning paper (IOUs) into a special paper. Later, they formalized the process by setting up a financial system to support it – Lo and Behold – the adoption and use of cash was borne.

Some progressive nations have shown genuine and committed interest in testing the viability of CBDCs. Seven Central Banks in October issued a statement in which they said they were studying common principles and salient features needed for a viable CBDC.

The Central Banks in Canada, Britain, the European Union, Japan, Switzerland, Sweden, and the United States now believe there is a threat that private digital currencies pose to the control of monetary policy.

More specifically, they are also competing with China, who they purposefully excluded from their group. They plan to have a viable digital currency system to prevent a case in which China gets the first-mover advantage.

Ad: Crypto

Advantages of CBDCs

We want to create a more efficient payment system. Managing cash can cost money mostly because of securing the safe use of it. We can include more people in a financial system as there is no need for consumers to have a bank account to hold a CBDC.

Safety is, therefore, a huge “positive” to having a cashless society. This is especially in emerging countries where many people still use cash as opposed to cards and electronic transfers (ETFs). Cash is trusted while banks aren’t necessarily trusted at all. Consumers also might not want to pay fees to keep their bank accounts open.

One salient case for a contactless (digital) payment system would is due to the advent of the Covid-19 virus. This has awakened us to the potential emergence and spreading of potential viruses in the future.

CBDC might also make micropayments cheaper which would allow for new services and business models. So, one can enable the efficient sale parts of products and services, such as individual news articles or television series episodes for a few cents rather than relying on subscription models.

A CBDC may also reduce friction between payment systems and increase the speed of transactions while ensuring their finality. This can be achieved by achieving delivery versus payment in securities transactions.

Interest-bearing retail CBDC might boost monetary policy efficiency. CBDC can provide a Central Bank with an additional financial instrument – the rate of interest it carries. CBDCs would provide competition to stable coin exchanges such as Bitcoin and Facebook’s Libra.

Issues with digital currencies & CBDCs

Cryptocurrencies currently exhibit huge swings in value (volatility) as people use them as a speculative asset. This could change if they were somehow monitored and administered by Central Banks.

The disintermediation of commercial banks would occur if consumers move money from bank accounts into CBDC. This could start a vicious cycle as banks raise deposit rates to attract more money and less bank credit will be extended at these higher interest rates.

A Central Bank could need to provide additional liquidity to banks and hence take on credit risk. There could be an increased reputational risk for Central Banks. Digital systems need to be protected and the system’s staff monitored.

Many questions remain unanswered

Cross border transactions will also create new paradigms for central banks. There are risks of a type of dollarisation for economies with volatile exchange ranges and high inflation.

‘Dollarization‘ is when a country replaces its currency with the US dollar because the dollar is so stable and widely used. In the foreseeable future countries may then opt to replace paper money with the best (continental) CBDC available – like a digital Euro for the EU.

The future depends on the goals of the CBDC. It would grant the public access to the state’s balance sheet when, right now, cash is the only way for private individuals to hold central bank money. All other types of money holdings are based on centralized/private money creation systems. These are still prone to manipulation and abuse by central banks themselves or their subsidiaries.

Did you know that there are still more than 700 million people in the world who live in extreme poverty? These people must scrimp, starve, and struggle to survive off less than $1.90 per day.

By 2030, the World Bank estimates that more than 90 percent of those people will be concentrated in Sub-Saharan Africa.

This is perhaps one of the greatest developmental failures of the modern world. Despite the continent’s expansive natural resources and increasing connectivity, foreign actors still feel it’s too risky to heavily invest in their markets.

Blockchain could be the key!

Bitcoin and “Blockchain” were created in the mass wave of distrust in banks after the 2008 financial crisis. Therefore, the technology enables individual, distributed data storage that could become the perfect evidence (trust) base and financial infrastructure for a developing country.

With the right implementation, Blockchain holds the potential to completely revolutionize and revitalize such economies, especially in Sub-Saharan Africa.

So, what is this Blockchain?

Blockchain is essentially a kind of decentralized database that allows you to have a safe, secure way to handle their data without the need for third parties.

For example, you could with Bitcoin, make or accept payments in real-time without needing a centralized bank.

“[It is] a way for one Internet user to transfer a unique piece of digital property to another Internet user, such that the transfer is guaranteed to be safe and secure, everyone knows that the transfer has taken place, and nobody can challenge the legitimacy of the transfer,” said software entrepreneur Marc Andreessen.

“The consequences of this breakthrough are hard to overstate.”

Historic background

Until the mid-twentieth century, most of Africa was ruled under a colonial system meant to exploit the people and their natural resources for European benefit. Africans, in addition, were rushed into development according to European standards rather than homegrown ones.

The legacy of rapid development, distrust and corruption left behind an economic system failing to recover in the 21st century.

While the World Bank celebrates a decrease in global poverty levels, the number is expected to remain stagnant in Africa. Today’s poorest people are living in places with the least economic growth.

Sadly enough, poverty and lack of investment in many developing countries stem from how they were integrated into the world system.

The land was cut into countries according to European treaties and agreements, rather than by traditional and tribal land divisions. This situation worsened upon the handover of colonial power to so-called “democracies.” Power often shifted to the ethnic groups that former colonizers favoured.

Corruption multiplied in the form of bribes, political persecution, rigged elections, and a massive wealth gap. All of this still affects the wealth distribution and investment potentials of many developing countries.

Of course, this created a lack of trust in banks and government throughout much of Sub-Saharan Africa.

The perfect fit for Africa

During a 2012 study conducted in rural Western Kenya, Stanford University researchers waived the costs of opening basic savings accounts for a number of unbanked individuals.

While 63 percent of the subjects opened an account, only 18 percent of them used the accounts. This was likely due to three factors: a lack of trust in banks, unreliable service and prohibitive withdrawal fees.

Unfortunately, the prevalence of unbanked individuals in the informal sectors scares off foreign investors, who heavily rely on transactional evidence to make investments. Otherwise, pouring money into markets is too risky. That’s where Blockchain comes in.

How would it work?

Blockchain can host an entire evidence base of transactions, loan repayments, and asset titles. The technology is also decentralized and requires individual confirmation, creating an element of trust and transparency beyond traditional banking systems.

According to Victor Olorunfemi, Director of Products for Pan-African tech and crypto-exchange, KuBitX, Blockchain’s major benefits lie in “frictionless P2P and cross-border payments, transparent elections, land registry management [and] transparent crowdfunding.”

Let’s look at some of the different ways Blockchain could benefit developing economies, especially in Sub-Saharan Africa.

1. Creating financial infrastructure and accountability

According to a study by the Milken Institute, viable financial markets require consistent, accurate data on assets and credit histories. Luckily, Blockchain may fulfil these needs.

The use of Smart Contracts technology is ideal in areas lacking accountability, such as the real estate or land/agricultural sectors. In Africa, a lack of record-keeping practices often leads to “missing” or non-existent title deeds. In some cases, this is intentional.

Title deeds “go missing,” only to end up in the hands of benefactors other than the rightful owners. Smart Contracts could eradicate these issues through the use of special tokens that cannot be duplicated, changed or removed. See the article on tokenization.

Likewise, Bitland, a company in Ghana, currently helps individuals record deeds and land surveys. By resolving land disputes, Bitland creates more stability while accurately recording land asset data.

“There’s a massive number of people in the informal sector, but there’s not much data being collected on them right now.”

Merit Webster, co-president of the MIT Sloan Africa Business Club.

“That means you don’t have that credit history or payment history for them. If you have a decentralized approach to collecting data, you end up with more malleable data. [This] is very valuable for creating credit histories.” The agricultural industry also has the potential to thrive using Blockchain.

“Blockchain could be used to track goods around the world. This allows farmers to earn a fair wage for their goods.”

Also, farmers could use record-keeping technology to streamline the supply chain and document resources. This would lead to better efficiency, lower transactional costs, and improved logistics.

2. Security in banking

According to the World Bank, there were 1.7 billion people with no bank account in 2017. This situation is worst in developing countries, especially African ones. For example, over 62 million of these people lived in Nigeria.

Besides, data from Google Trends reveal that Lagos, one of Nigeria’s biggest cities, ranks globally as the number one city based on the volume of online searches for Bitcoin (BTC). Clearly, for the city’s 21 million-odd people, there an immense interest in some form of an accessible payment system.

Of course, it’s unrealistic to expect bank branches to magically appear in every remote corner of the world. However, a digital database using Blockchain technologies has the potential to reach far beyond physical banks.

Ad: N26 Bank

Many Africans value trust and transparency. In developing countries, this lack of trust goes beyond the Internet. Developing countries with less industrialization tend to have higher levels of corruption.

This reduces national investment opportunities in the public sector and instills a lack of trust in centralized oligarchs handling an international investment.

Because its power lies within the community of users, Blockchain can combat these trust issues. All data logs and amendments must pass through this community and identification confirmation tests.

Blockchain technology also secures your data incredibly. Hacking and data breaches are all too common nowadays. In 2017, for example, around 3 billion Yahoo user accounts were stolen.

When information is stored in the same place, hackers have one, easy target. In contrast, Blockchain is a distributed entity. This dissemination of data leaves it far less vulnerable to cyberattacks.

3. Fostering Entrepreneurship

Coupled with the Internet, Blockchain technology could be the perfect platform for aspiring African developers. Because the ‘source code’ is free of charge, skilled coders can adapt, create, and configure special applications, called DApps.

These are available on Crypto platforms and provided by companies like Ethereum, and a South African firm specializing in what they called the Keto-Coin.

Rather than waiting for governments to drag their feet trying to create jobs—individuals on the continent can form small firms that build and sell Crypto-based Apps locally or abroad.

“Despite the frictions and impediments mentioned,” said Olorunfemi. “Blockchain can still provide an avenue for promising African tech projects to access capital (FDI) via token offerings on digital assets exchanges.”

Many courses are even readily available online to quickly learn about new technology. Microsoft, for instance, offers a platform via Azure for you to build and learn about the Blockchain.

One-man shops in countries with unfavourable economic systems, like Zimbabwe, can also adopt smaller, stable, Cryptocurrencies to facilitate or payments. In cases of rampant inflation, they can temporarily act as a store of value or help you pay for things until your currency stabilizes.

As with the Venezuelan hyperinflation case study, Cryptocurrency intervention could help many developing countries troubled with economic instability.

There is also the option of Crypto-mining. But before you pull out the ‘high-consumption energy’ argument – think outside the box for a moment. What about energy sources that are free and available nearly 24/7? Like water and the sun!

The African continent is full of capable scientists and mechanical engineers. One could build special solar-powered energy centers to power Bitcoin-mining.

And without the expertise, governments or private companies could alternatively just invite Crypto companies with abundant financial resources to mine (cleanly) for a special tax/fee while creating jobs for the locals.

4. Elections

In addition to the financial side of things, Blockchain technology could help eliminate some forms of corruption. For example, many African countries’ elections are incredibly vulnerable to the social scourge. In some extreme cases, some officials change or forge written ballot votes to rig elections.

To combat this, Blockchain databases could record votes. This makes it nearly impossible to tamper with using Smart Contract technology. Having fair elections improves infrastructure, which then increases development and economic dependability.

While some might see Africa’s economy as underdeveloped, others might see it as a blank canvas well-suited for a large-scale implementation of Blockchain. Economic and governmental systems are shifting and slightly shaky in many Sub-Saharan African nations.

The challenge is to foster a rigid economic system to implement Blockchain.

Don’t just take our word for it—African nations have often implemented new, practical technologies before the Western world. Let’s look at the example of M-Pesa. Back in 2014, Americans and Europeans were amazed by Apple Pay’s launch.

However, this mobile payment system wasn’t exactly “new.” By that time, Kenyans had used M-Pesa, a very similar technology, for years.

“There’s a lot of opportunity to leapfrog the way the West developed and have these more unique African solutions, but it needs to come from within,” said Webster.

“It needs to come from entrepreneurs in the continent who want to implement these solutions. It’s important to engage people very early on. Systems incubated in the West don’t stand as great of a chance to work as African ones do.”

Concluding remarks

With the possibility of an experimental, large-scale takeover of Blockchain technology to improve African infrastructure, the nations there could leapfrog in development and growth.

This must begin internally. According to Olorunfemi, “Education—of policymakers and other stakeholders—which is often ignored has to be a critical factor in paving the way for the acceptance and adoption of new technologies and the accompanying investment.”

The results in Sub-Saharan African countries could help eliminate much of the world’s poverty. It would also remove remnants of mistrust and corruption left behind by the days of colonial exploitation.

While there are some obstacles to large-scale Blockchain implementation, we can’t think of a better benefactor than there. The possibilities for business using the Blockchain are endless!

To learn more about how to get started with Cryptocurrency mining or purchasing, visit our resources page for useful links and guides.

Additional input by Bobby Quarshie (BQ).

Citations: Christopher Lee and Jackson Mueller.

Swan, Melanie. “Anticipating the Economic Benefits of Blockchain.” Technology Innovation Management Review 7.10. Oct. 2017.

Bitcoin Lessons from Venezuela, Where Hyperinflation Reigns. Online Source: https://www.lathropgage.com/newsletter-237.html

We end the year once more with trading: a topic that might not be directly tech-related. It, however, relies heavily on online technology to help with investments and therefore, is noteworthy.

More and more millennials are getting into the habit of adopting get-rich schemes. You just have to look on Instagram and Twitter to see how gullible some of them are to Ponzi-like schemes preying on online and financial naivety.

It has become so cumbersome as most of the predators ‘befriend’ you only to present you with the offer to trade (Forex, Binary options, or mine Crypto) on your behalf. Some blatantly just ask for you to deposit cash (usual increments of $500) into unknown accounts!

Nothing to perform due diligence is available and not even a website sometimes – just the promise of profits of up to 30-80% weekly, monthly, or whatever – it’s all clickbait!

A notable 60 percent of high net worth individuals (HNWIs) in Latin America alone showed high-interest levels in Crypto investments in 2018.

Capgemini’s World Wealth Report 2018.

You can, however, as we mentioned around this time last year, take full control of your financial destiny.

When it comes to managing an online portfolio via a broker such IQOption, there are a few things you have to consider first before dropping cash into your trading account.

Checklist

Research

Equities (Shares or stocks, ETFs, Commodities, Indices, Options, Forex, Futures, and Cryptocurrency). These are all vehicles you can engage with concurrently in the same portfolio. They all also have their (moderate to extremely high)levels of risk. Learn how each of them works. Shares are actually the less risky of the batch nowadays.

Have a plan! One does not just opt to invest in equities to “make money”. Of course, you will make (or lose) money. The question is how much and within what timeframe? When are you looking to have the money back? These questions will help determine what kind of investor you are or the approach to adopt when investing.

Based on your knowledge, appetite for risk, and the associated costs, you will either be a long, mid (mixed), or short-term investor. The latter is referred more commonly to as day-trading. Long term trading works pretty much like savings. You buy the stock/share and hold it for a long period of time (shares/stocks and indices are the best vehicles for such). All the others can be bought and sold by the minute, hour, day, or weekly.

Setting up

Setting up with your bank means there is also less admin when it comes to verifying your personal details such as ID, physical address, and so on.

Be sure to have all documents ready and up to date. These are mandatory and required by local financial authorities to help prevent or determine fraud, the use of securities to launder money, or fund terrorism.

The bank trading brokerage fee can be waivered by going for an online broker independently if you have all your ducks (paperwork) in a row.

Costs

Once set up, there are further internal costs that the broker will charge you. Pay attention to the commission charged when you purchase security of choice. Some waiver it but then charge what is called a spread. Then there are other deductions such as a charge for borrowing money to trade – what is termed ‘overnight fees‘.

And of course – pay attention to TAX!

Pay attention to all the associated costs. It costs nothing to setup an online trading account via a broker. Your bank may charge a brokerage fee for running a separate trading account. The advantage of that mainly is just the ease of adding and withdrawing your ‘winnings’.

We strongly recommend actively running a trial for at least 2 monthsbefore making your first deposit to start purchasing securities.

Some strategies

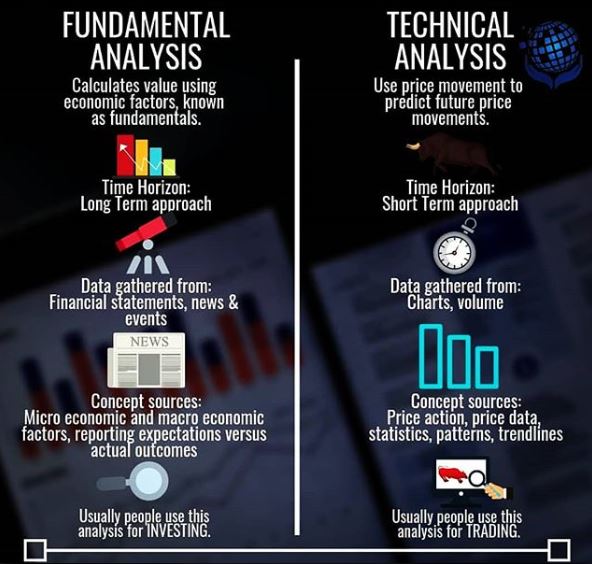

Before that first purchase, you should hopefully, by then, have used the trial period to learn some of the tools. Trading (or investing) is not something you do out of a gut feeling. There is about 3% ‘gut feel’ but the rest of the knowledge comes from studying the tools for technical and fundamental analysis.

The difference between technical and fundamental analysis is the difference between trading and investing – without any, you are outright just gambling!

There are also some ways to mitigate your risk and minimize losses. One system that applies to all investing is called Dollar-Cost-Averaging. So, under this strategy, you divide the total amount into bits to ensure that on average your losses are smoothed out by profits. The diagram to the left illustrates this.

Budget within your portfolio

Always start small and see how that goes before diving fully in. People get greedy and think if $10 fetches a $5 profit then $10 000 would subsequently garner $5000 or at least $500. It doesn’t always pan out that way. If it was that easy we would all be millionaires!

One must also quickly avoid the habit of topping up the account to get the next hot stock because like a business, your trading portfolio is an investment for future growth. It must therefore, be nurtured that way.

Ride the waves (with your initial investment) and reinvest your winnings by ploughing back some of the profits into less riskier securities once you make a small ‘killing’.

Switch from a short to medium term trading approach to secure your profits. Many day traders end up losing all their gains because they stay in the game for too long. The stock market always turns eventually and gets its pound of flesh!

As a rule of thumb, purchase only after a massive drop in price – as you would in a fashion sale. When a security’s price has risen to abnormally high levels, its ‘bubble’ tends to ‘burst’. In addition, there are tools to measure whether a stock/share or any security for that matter is overvalued. Study them!

Market trends

The markets are constantly in motion and like a rollercoaster, prices are constantly going up and down. You have to choose where (and when) to place your buys (and positions) to make your profits.

Know the market (opening and closing) times so you do not miss a good deal. Many markets will either open with a big rally; cool off in the afternoon and then close with a sell-off (in the red) in the evenings in general.

What causes the up and downs is the buying and selling off respectively.

Based on that, and with the common knowledge that everyone sells at a high profit – what do you then think would happen after a massive rise in the price of a security? It is not rocket-science yet many people fall for it and end up buying at the height (peak) price of an equity.

Easier said than done. Naturally, it is hard to predict where this peak is as many inexperienced profit hunters have found out the hard way.

Markets tend to crash in predictable cycles. The Crypto market fell by a whopping 70% in 2018 – a monumental drop in market capitalization after its equally amazing 2-month bull run. Many individuals and companies who bought Cryptos in January 2018 as a result went down in flames because of such bad timing – and just plain greed.

These are just some of the basics to help you get into an investing state of mind – more particularly with online trading. You will find a few more useful pieces of information on the resources page.

Happy trading and remember to start of with a free trial!

General Risk Warning: The financial products offered by the company carry a high level of risk and can result in the loss of all your funds. You should never invest money that you cannot afford to lose.

We have barely scratched the surface with the Internet (from the early eighties) and it is already seemingly being threatened with the competition. A possible replacement by a new phenomenon.

Well, for lack of a better word, “replaced” has connotations of a dying Internet. This is far from accurate. This new phenomenon – fostered by blockchain technology, will change the way we use and consume the Internet as a service.

So, what is this new Internet-like system creating waves online? And why is it making online marketers quiver at the prospect of them losing out on the exponential revenues they have previously enjoyed?

Before we delve further into its meaning and use in the cyber world, perhaps some background context is required.

The way we use online or mobile applications software or “Apps” has changed how we consume products and services online. Companies jumped onto the bandwagon when they discovered that we mostly use Smartphones for the Internet.

App developers were then subsequently sought after to create mobile Apps for practically anything. What started as something mainly for gamers moved quickly onto applications for practically any commercial activity.

We now use Apps for our shopping; fitness; traveling; online bookings and banking. Developers now create customized software to help us with practically, anything.

In addition, we now have App stores for every significant tech provider – Microsoft, Google, and Apple to mention a few. This has naturally fattened the pockets of software companies and created an additional stream of income for them.

The ‘catch’ for using mobile apps is that even though it costs you nothing to download, using them still requires you to register with your personal details. You can also do this by linkingyour existing social media accounts.

The benefit to App providers

These Apps, which are integrated with social media services, create a data goldmine for marketers to study and track browsing habits. Through them, marketers can gain valuable insights into your interests and then customize their products/services to sell to you.

The impetus behind a distributed application system is that it serves to distribute plow some of the wealth garnered from your data via application providers back to you.

Data mining has become more lucrative and accessible because of Artificial Intelligence (AI) and Machine Learning. Do you ever notice how after browsing online or having a conversation or a chat application like WhatsApp or Facebook Messenger? You go online later, and you see Ads displaying the items you discussed? Creepy isn’t it? Well, that is the future of Web 4.0 for you!

Staying ‘woke’

Luckily for us, there is a school of knowledgeable and security-conscious programmers who are not ‘giving in’. They help us understand how the Internet has become a cesspool for marketers to harvest our data. Social media platforms, search engine providers, and mobile application providers facilitate them immensely with this.

Imagine getting paid to surf the web for hours. The way you get paid for taking on a survey, partaking in a social experiment, donating an organ or sperm?

This is the way distributed apps are touted to work. They reward you for the use of specific applications (in a peer-to-peer review setting) with cashable tokens. Seems only fair right?

Now you can imagine how companies like Cambridge Analytica would react to having to pay you for their use of your data. They would surely be reluctant and that’s why they preferred to work clandestinely. But if they could pay companies like Facebook for the use of data, why not pay us directly?

Early adoption

Joining the ‘DApps revolution’ is a no-brainer. Those at the forefront of building and supporting DApps will end up with a more substantial chunk of the market.

DApps primarily provide you with the use of payment systems. These are specifically known as Smart Contracts and Proof of Work systems.

For instance, you are rewarded in cashable tokens to surf the net over applications like Google Chrome, or Mozilla Firefox.

It is only a matter of time that this form of Internet-browsing and use of applications becomes the norm.

The Internet revolutionized the way we communicate, socialize, learn, shop, and do business online. DApps however, will determine the way you get compensated for doing the things you love to do online.

When it comes to providing means of storing, sending, and receiving money, banks and their affiliated institutions, have enjoyed a monopoly for centuries.

They (especially central banks which allegedly are owned powerful families) have the authority to influence countries and their governments. We will not go into the level of control as this paves the way for conspiracy theories which though not proven – are not farfetched.

So, it’s only expected that when some new and unknown entity threatens their prosperity, they start to react.

Blockchain frenzy

How banks are responding is evident by how they are fervently building their own blockchains. This, however, defeats the purpose of a having decentralized system.

Bitcoin and cryptocurrencies get their appeal not just because they are very secure. But because unlike fiat money, they are not heavily regulated and can be mathematically restricted.

The 21 million unit limit on Bitcoin by default places it closer to the status of gold (which is also not infinite). But what happens when all are mined in 2041? Bitcoin’s current ‘value’ of over $30 000 (adjusted),could move up again, according to the traditional laws of supply and demand as it becomes rare.

To unlock more value the creators will split it again. The first major splits (forks) gave rise to Litecoin and Bitcoin Cash. Both cryptocurrencies are racing to newer heights daily.

How banks operate

Now back to the banks – they make money from our deposits and these deposits are backed up by our reserve banks. Reserve banks lend retail banks money which they essentially just print. The banks must ‘turn it’ and pay it back with interest (repo rate).

So, technically we ‘empower’ banks by depositing our money so they can invest the funds in all sorts of mechanisms. Such mechanisms include the credit and loans to you, your businesses, equities, and property.

Then, they also invest in high-risk investment vehicles like currency trading, derivatives (futures). They are essentially the biggest regulated and legal Ponzi-schemes. They also make a significant amount of the daily fees they charge you.

A quick example

Let’s quickly put things into context. A bank with over a million customers transacting daily. Let’s say they charge you a 10 cent (conservative figure) transaction fee for depositing, withdrawing from another bank, or an intra-bank transfer.

They then make 0.10c x 1 000 000 = 100 000 units of the currency on the day. This equates to 1,2 million Euros, Dollars, Rands, or Yen annually. And that is just off your transactional fees!

Then they also charge you monthly service/maintenance fees. Those are to cover the convenience of you having an account and, for services like online banking.

This is what cryptocurrencies can potentially wipe away from banks we all go the digital currencies route. Granted, how you acquire and transfer Cryptocurrencies are not as straightforward as receiving paper money – yet.

That, coupled with the stigma around ‘Cryptos’, means there is still a barrier to entry for the ‘open-source’ monetary system.

Banks will try and bring about their own blockchains to address security concerns around making transactions. For them, however, it would still be business as usual when it comes to the charges.

Birth of Fintech

Some newer financial institutions, however, are already progressing in the favour of you and me – one such is the European based N26 Bank.

We often end up paying for things all month without even having to go to an ATM. It works as a traditional bank would, however, allows the (smart) card to be used as a credit card (backed by Mastercard) would.

This allows you to quickly purchase goods online, book events, flights ticket, and accommodation. Basically, all things you still can’t do with your debit card.

In countries like Sweden and Estonia, card and digital systems have been a thing for a long time now.

Some of these Fintechs are adopting or partnering with Cryptos companies to deliver their services. One such as the relationship the one between a German bank and the crypto Ripple.

Click image topurchaseRipple here

It would be interesting to see what governments and financial institutions do to ‘protect’ their payment systems. Likewise, it will be equally fascinating to observe how they adapt in general to the new digital era upon us.

Translate »

This website uses cookies. By continuing to use this site, you accept our use of cookies.